From Experiments to Priors: Eliciting Informative Priors for Your Marketing Mix Model

MMM

python

prior elicitation

experimentation

media mix modeling

bayesian

pymc

causalpy

synthetic control

How to translate quasi-experimental results into informative Bayesian priors for your MMM using CausalPy and PyMC-Marketing.

Introduction

If you’ve worked with Marketing Mix Models long enough, you’ve heard the term calibration — the idea that models alone aren’t enough and that external evidence should sharpen their estimates. In PyMC-Marketing, calibration already has a precise meaning: the add_lift_test_measurements method adds experimental observations directly to the model likelihood, treating them as additional data the model must explain during sampling.

But there is another way to let experiments inform your model — one that operates at a different stage of Bayesian inference. Instead of enriching the likelihood, we can use experimental results to elicit informative priors on the saturation parameters (see the callout below for the precise distinction).

Before diving in, let’s ground ourselves in the core objective of any marketing measurement strategy: understanding the incremental impact of campaigns and actions. The pursuit of that answer gave rise to cookies, pixels, and a zoo of user-level identifiers on the web. Now, as those tools fade under heightened privacy regulation, new statistical methods have emerged to fill the gap.

Marketing Mix Modeling, together with randomised and quasi-experiments, are the leading contenders. Yet measuring how advertising shapes human decisions is inherently hard. The methodology you choose — and the conditions under which you apply it — can lead to very different readings of reality.

How can we align models that measure different facets of the same multifaceted phenomenon? Can we consolidate prior knowledge from experiments into a single, principled methodology?

This article explores prior elicitation from experiments — a fully Bayesian pipeline that translates causal evidence into informative priors, propagating uncertainty end to end. We’ll use the latest multidimensional MMM API from PyMC-Marketing and CausalPy for the causal inference piece.

Prior elicitation vs likelihood calibration

PyMC-Marketing’s add_lift_test_measurements incorporates experimental evidence as an additional likelihood term — the experiment becomes observed data that the model must explain during sampling. This is calibration in the strict sense: experimental observations enter P(\text{data} \mid \theta).

The approach in this article is different. We use the experimental result to elicit informative priors on the saturation parameters. A small Bayesian model translates the experimental observation into a full posterior over (\alpha, \lambda), which then becomes the prior for the MMM. The experimental knowledge enters through P(\theta).

Both approaches are valid and complementary. Likelihood calibration is powerful when you have multiple lift tests and want them to directly constrain the model during inference. Prior elicitation is valuable when you want to encode experimental knowledge as prior beliefs — preserving the distinction between what you know before seeing the time series and what the time series itself teaches you.

This article walks you through:

- Setting up a Synthetic Control quasi-experiment with CausalPy to estimate a specific causal effect.

- Translating the experimental result into the derivative space of our saturation function.

- Building a small PyMC prior elicitation model that turns the experimental observation into a full posterior over saturation parameters.

- Using that elicitation posterior as informative priors in the multidimensional MMM from

pymc-marketing. - Comparing a generic (default-prior) model against the experiment-informed model.

Business case

Imagine this: your company decides to dial back its advertising budget in Venezuela between late March and early May. As a marketer you’re scratching your head — did this hurt sales? If so, by how much?

Before reaching for complex techniques, let’s think about how to measure this specific action. We can unravel the mystery through the power of experiments.

Although spending dropped in Venezuela, the company maintained its usual advertising in other countries. This gives us a unique chance to peek into an alternate reality — what would have happened if the spending hadn’t been cut?

Let’s pick Colombia — a country where advertising continued unchanged during the same period — as our control group. Why Colombia? The hypothesis is that Venezuela and Colombia are exposed to similar macro-economic factors: both sit in the north of South America, share similar climates and culturally overlapping populations, and were literally the same country less than two centuries ago. We can treat them as representatively similar.

\text{Venezuela Sales} = \text{Colombia Sales} \cdot \beta + \text{Venezuela Exogenous Variables}

If we assume this relationship, we get the following causal structure:

- Shared factors (weather, seasonality, macro-trends) drive both countries’ sales.

- Country-specific exogenous variables affect only one country.

- During the treatment window, Venezuela’s media spend drops — but Colombia’s does not.

Note

This methodology isn’t limited to countries. It works equally well for regions or cities, as long as you have consistent assumptions supported by data. Also, the control time series should not be affected by the intervention being measured. We are not considering spill-over effects here.

By comparing the two realities — observed Venezuela (treatment) versus counterfactual Venezuela (estimated via Colombia) — we can directly measure what was lost by stopping marketing. And this is precisely the kind of evidence that, when translated into informative Bayesian priors, makes our Media Mix Model substantially more accurate.

Time to meet your go-to tool for this job: CausalPy.

CausalPy is a library from the PyMC ecosystem designed to facilitate causal inference analyses. Using CausalPy we can explore different quasi-experimental methods to causally measure the effect of our actions in the absence of natural or randomised experiments.

Let’s jump into action.

Getting started

This notebook assumes familiarity with the essentials of PyMC-Marketing. If you’re new, the Marketing Mix Modeling example notebook is an excellent starting point. Before we begin, make sure you have both libraries installed:

Installation command

pip install pymc-marketing causalpy

We’ll start by importing the necessary libraries for Bayesian modeling, causal inference, and visualization.

Code

import warnings

warnings.filterwarnings("ignore")

# Domain-specific / PyMC ecosystem

from pymc_marketing.mmm import GeometricAdstock, MichaelisMentenSaturation

from pymc_marketing.mmm.multidimensional import MMM

from pymc_extras.prior import Prior

import causalpy as cp

import pymc as pm

import arviz as az

import preliz as pz

# Visualization

import matplotlib.pyplot as plt

import seaborn as sns

# Scientific computing

import numpy as np

import pandas as pd

from scipy import stats as sp_stats

# PyTensor (automatic differentiation)

import pytensor

import pytensor.tensor as pt

from pytensor import function as pytensor_function

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [8, 4]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["axes.labelsize"] = 6

plt.rcParams["xtick.labelsize"] = 6

plt.rcParams["ytick.labelsize"] = 6

plt.rcParams.update({"figure.constrained_layout.use": True})

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"

seed: int = sum(map(ord, "calibrating mmm with experiments"))

rng: np.random.Generator = np.random.default_rng(seed=seed)

pd.DataFrame({"seed": [seed]}).head()| seed | |

|---|---|

| 0 | 3223 |

Understanding our dataset

We’ll build a synthetic dataset so the entire analysis is self-contained and reproducible. The data mimics a realistic marketing scenario with two countries and two advertising channels.

The ground-truth parameters we embed in the data-generation process will later serve as our benchmark for evaluating how well experiment-informed priors recover reality.

Code

n_weeks: int = 150

min_date = pd.to_datetime("2021-01-01")

date_range = pd.date_range(start=min_date, periods=n_weeks, freq="W")

df = pd.DataFrame(data={"ds": date_range}).assign(

year=lambda x: x["ds"].dt.year,

week=lambda x: x["ds"].dt.isocalendar().week.astype(int),

)

n = df.shape[0]

pd.DataFrame({"n_observations": [n]}).head()| n_observations | |

|---|---|

| 0 | 150 |

Now let’s define the true parameters that govern the relationship between media spend and sales. We’ll use the Michaelis-Menten saturation function:

f(x) = \frac{\alpha \cdot x}{\lambda + x}

where:

- \alpha is the maximum achievable effect (the asymptote)

- \lambda is the half-saturation point (the spend level at which we reach half the maximum effect)

Code

# True saturation parameters

TRUE_ALPHA_META: float = 2.75

TRUE_LAM_META: float = 2.50

TRUE_ALPHA_GOOGLE: float = 2.00

TRUE_LAM_GOOGLE: float = 3.00

# True adstock parameter (geometric decay)

TRUE_ADSTOCK_ALPHA_META: float = 0.6

TRUE_ADSTOCK_ALPHA_GOOGLE: float = 0.4

# Intercept and scale

INTERCEPT: float = 3.0

# Reusable instances for the data-generation process

dgp_adstock = GeometricAdstock(l_max=4)

dgp_saturation = MichaelisMentenSaturation()Let’s generate the media spend for each channel. We smooth the raw samples with a convolution to get realistic-looking weekly spend patterns.

Code

SMOOTHING_WINDOW: int = 8

# Meta spend (with a treatment dip in Venezuela)

pz_meta_raw = pz.Gamma(mu=3, sigma=1).rvs(n, random_state=rng)

pz_meta_smooth = np.convolve(pz_meta_raw, np.ones(SMOOTHING_WINDOW) / SMOOTHING_WINDOW, mode="same")

pz_meta_smooth[:SMOOTHING_WINDOW] = pz_meta_smooth[SMOOTHING_WINDOW:2 * SMOOTHING_WINDOW].mean()

pz_meta_smooth[-SMOOTHING_WINDOW:] = pz_meta_smooth[-2 * SMOOTHING_WINDOW:-SMOOTHING_WINDOW].mean()

# Google spend (unchanged throughout)

pz_google_raw = pz.Gamma(mu=2, sigma=0.8).rvs(n, random_state=rng)

pz_google_smooth = np.convolve(pz_google_raw, np.ones(SMOOTHING_WINDOW) / SMOOTHING_WINDOW, mode="same")

pz_google_smooth[:SMOOTHING_WINDOW] = pz_google_smooth[SMOOTHING_WINDOW:2 * SMOOTHING_WINDOW].mean()

pz_google_smooth[-SMOOTHING_WINDOW:] = pz_google_smooth[-2 * SMOOTHING_WINDOW:-SMOOTHING_WINDOW].mean()

# Trend component

trend = np.linspace(0, 0.5, n)

# Seasonality component

seasonality = 0.3 * np.sin(2 * np.pi * np.arange(n) / 52)

# Shared base for both countries

shared_base = INTERCEPT + trend + seasonality

start_date = pd.to_datetime("2021-09-26")

end_date = pd.to_datetime("2021-11-28")

treatment_mask = (date_range >= start_date) & (date_range <= end_date)

# Venezuela meta spend: drops during treatment

meta_venezuela = pz_meta_smooth.copy()

meta_venezuela[treatment_mask] *= 0.1 # 90% reduction

# Apply adstock + saturation with TRUE parameters

meta_ve_adstocked = dgp_adstock.function(x=meta_venezuela, alpha=TRUE_ADSTOCK_ALPHA_META).eval()

meta_ve_saturated = dgp_saturation.function(x=meta_ve_adstocked, alpha=TRUE_ALPHA_META, lam=TRUE_LAM_META).eval()

google_adstocked = dgp_adstock.function(x=pz_google_smooth, alpha=TRUE_ADSTOCK_ALPHA_GOOGLE).eval()

google_saturated = dgp_saturation.function(x=google_adstocked, alpha=TRUE_ALPHA_GOOGLE, lam=TRUE_LAM_GOOGLE).eval()

# Colombia: same media but NO treatment reduction

meta_co_adstocked = dgp_adstock.function(x=pz_meta_smooth, alpha=TRUE_ADSTOCK_ALPHA_META).eval()

meta_co_saturated = dgp_saturation.function(x=meta_co_adstocked, alpha=TRUE_ALPHA_META * 0.9, lam=TRUE_LAM_META * 1.1).eval()

google_co_saturated = dgp_saturation.function(x=google_adstocked, alpha=TRUE_ALPHA_GOOGLE * 0.85, lam=TRUE_LAM_GOOGLE * 1.05).eval()

# Noise

noise_ve = pz.Normal(0, 0.15).rvs(n, random_state=rng)

noise_co = pz.Normal(0, 0.15).rvs(n, random_state=np.random.default_rng(seed + 1))

# Sales

venezuela_sales = shared_base + meta_ve_saturated + google_saturated + noise_ve

colombia_sales = shared_base * 1.05 + meta_co_saturated + google_co_saturated + noise_co

# Assemble the DataFrame

df = df.assign(

venezuela=venezuela_sales,

colombia=colombia_sales,

meta=meta_venezuela,

google=pz_google_smooth,

trend=trend,

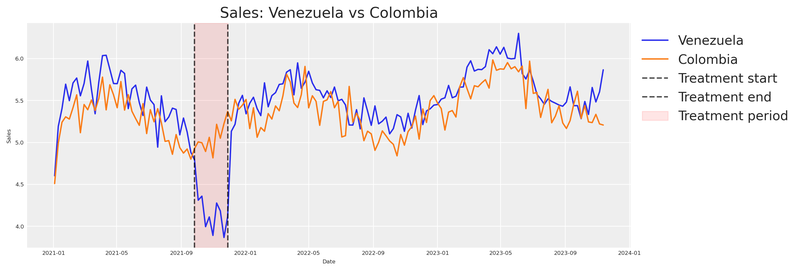

)Now for the critical part: Venezuela’s meta spend drops during the treatment window, while Colombia’s advertising continues unchanged. We need to verify that the two countries behave similarly enough to justify our counterfactual assumption.

Code

fig, ax = plt.subplots(figsize=(12, 4))

sns.lineplot(x="ds", y="venezuela", data=df, ax=ax, label="Venezuela", color="C0")

sns.lineplot(x="ds", y="colombia", data=df, ax=ax, label="Colombia", color="C1")

ax.axvline(start_date, color="black", linestyle="--", alpha=0.7, label="Treatment start")

ax.axvline(end_date, color="black", linestyle="--", alpha=0.7, label="Treatment end")

ax.axvspan(start_date, end_date, alpha=0.1, color="red", label="Treatment period")

ax.set(title="Sales: Venezuela vs Colombia", xlabel="Date", ylabel="Sales")

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

Notice how sales from Venezuela and Colombia move in sync until just before the intervention period (marked by the vertical lines), where Venezuela appears to dip while Colombia continues its normal trajectory.

Note

This visual alignment validates our hypothesis that both countries share common factors. If the two series were wildly different pre-treatment, we’d have no business using Colombia as a counterfactual.

We can see that something happened. But how do we quantify it?

Estimating the causal effect with CausalPy

Let’s turn to CausalPy’s SyntheticControl class. The idea is simple: build a synthetic version of Venezuela from the control unit (Colombia), then compare that synthetic counterfactual against what actually happened. The gap between the two is our causal effect.

The SyntheticControl class requires:

data: A DataFrame indexed by date with columns for each unit.treatment_time: The date at which the treatment was applied.control_units: The column names of the control (donor) units.treated_units: The column names of the treated units.model: A Bayesian weighting model (e.g.,WeightedSumFitter).

Code

experiment = cp.SyntheticControl(

df.query(f"ds<='{end_date}'").set_index("ds")[["venezuela", "colombia"]],

start_date,

control_units=["colombia"],

treated_units=["venezuela"],

model=cp.pymc_models.WeightedSumFitter(

sample_kwargs={

"random_seed": seed,

"target_accept": 0.95,

"draws": 250,

}

),

)

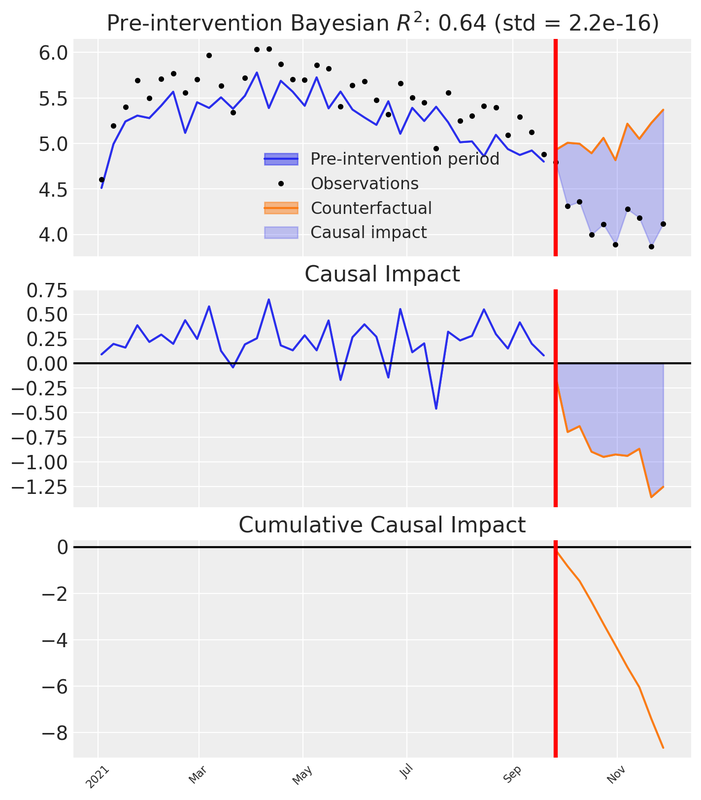

fig, ax = experiment.plot()

plt.xticks(rotation=45, fontsize=8)

plt.show()

Let’s unpack what we see in the three subplots:

Top panel: Observed Venezuela sales versus the synthetic counterfactual constructed from Colombia. Before the intervention the synthetic closely tracks reality; after the intervention a visible gap opens — the divergence between the synthetic and the observed.

Middle panel: The pointwise causal impact — the difference between observed and synthetic at each time step. Near zero pre-intervention; distinctly negative afterward.

Bottom panel: The cumulative causal impact — the running total of the pointwise differences over time.

These three views let us both visualise and quantify the impact of our action.

To attribute the observed change to our advertising reduction, we must ensure the model controls for all relevant factors. Our synthetic data was designed with this in mind (based on the DAG above), but in real-world situations you need to include additional donor units and covariates that account for confounders that might arise during an experiment.

Key principle

If there’s another plausible explanation for the change, we cannot confidently attribute it to our action.

Recommended reading for validating your causal model before the experiment:

We have the CausalPy result. Now we need to extract the total cumulative effect — the total delta lost due to our action — along with its uncertainty. Instead of collapsing the posterior into a single mean, we keep the full distribution across MCMC draws and compute the 95% Highest Density Interval (HDI).

Code

post_impact_unit = experiment.post_impact.isel(treated_units=0)

obs_dim = [d for d in post_impact_unit.dims if d not in ("chain", "draw")][0]

# Full posterior of total causal effect (sum of pointwise impacts per MCMC draw)

total_effect_per_draw = post_impact_unit.sum(dim=obs_dim)

total_effect_samples = total_effect_per_draw.values.flatten()

detected_effect = total_effect_samples.mean()

effect_hdi = az.hdi(total_effect_samples, hdi_prob=0.95)

detected_effect_lower, detected_effect_upper = effect_hdi

pd.DataFrame({

"Detected cumulative effect (mean)": [round(detected_effect, 2)],

"95% HDI lower": [round(detected_effect_lower, 2)],

"95% HDI upper": [round(detected_effect_upper, 2)],

}).head()| Detected cumulative effect (mean) | 95% HDI lower | 95% HDI upper | |

|---|---|---|---|

| 0 | -8.65 | -8.65 | -8.65 |

We’ve observed a decrease in Venezuela’s sales after reducing meta spend. This decline represents the lost delta contribution from our marketing activities. Crucially, the 95% HDI captures the uncertainty in that estimate — and we will carry this uncertainty all the way through to our prior distributions.

Now, this delta in sales was caused by a delta in advertising spending. To quantify the spend change we compare the counterfactual spend (what would have been spent without intervention) against the actual spend during the treatment window.

Code

# Counterfactual spend: average weekly meta spend before the intervention

pre_treatment_meta = df.loc[df["ds"] < start_date, "meta"]

counterfactual_spend_per_week = pre_treatment_meta.mean()

# Actual spend during the treatment (already reduced by ~90%)

treatment_meta = df.loc[treatment_mask, "meta"]

actual_spend_per_week = treatment_meta.mean()

n_treatment_weeks = int(treatment_mask.sum())

# Total spend reduction over the treatment window

total_delta_spend = (counterfactual_spend_per_week - actual_spend_per_week) * n_treatment_weeks

pd.DataFrame({

"Counterfactual spend/week": [round(counterfactual_spend_per_week, 4)],

"Actual spend/week": [round(actual_spend_per_week, 4)],

"Treatment weeks": [n_treatment_weeks],

"Total spend reduction": [round(total_delta_spend, 4)],

}).head()| Counterfactual spend/week | Actual spend/week | Treatment weeks | Total spend reduction | |

|---|---|---|---|---|

| 0 | 3.1395 | 0.3319 | 10 | 28.076 |

The total spend reduction over the treatment window, together with the cumulative sales impact, gives us a matched pair of deltas.

Assumption: stationary counterfactual spend

The counterfactual spend is estimated as the pre-treatment mean of meta spend. This assumes spending was approximately stationary before the intervention — i.e., there was no trend in meta spend. If spend was trending upward or downward before the treatment, the pre-treatment mean would under- or over-estimate the true counterfactual, biasing the \Delta X calculation. In practice, inspect the spend series for trends and consider using a trend-adjusted forecast if needed.

Important

The total spend reduction (\Delta X) and total sales impact (\Delta Y) form a single coordinate pair in the derivative space of our saturation function: the x-coordinate is the midpoint between counterfactual and actual spend levels, and the y-coordinate is the average rate of change \Delta Y / \Delta X.

This is excellent. With a single experiment we have a concrete estimate of incremental impact. But a single event at a specific moment doesn’t capture behaviour over time. The timing of our analysis influences the results.

This is precisely why we need a Marketing Mix Model — a methodological framework that lets us understand incremental effects over various periods. Experiments give us a prior anchor; the MMM gives us the full dynamic picture.

From experiment to saturation priors

To go from a single experimental observation to a full saturation curve, we need to understand the relationship between our variables.

Our assumption: marketing effects saturate following the Michaelis-Menten equation, and carryover follows a geometric decay. Under this assumption, the experimental data point — the change in Y given a change in X — lives somewhere on the derivative of our saturation function.

f(x) = \frac{\alpha \cdot x}{\lambda + x}

The derivative with respect to x:

f'(x) = \frac{\alpha \cdot \lambda}{(\lambda + x)^2}

This derivative tells us the rate of change on the Y axis for a given value on X.

Because MichaelisMentenSaturation.function() is built from standard PyTensor ops, we can use automatic differentiation (pt.grad) to compute the derivative — no manual formula required. We wrap this in a single saturation_derivative function that works in two contexts: pass a pt.dvector and compile it for fast numerical evaluation (plotting), or pass a pytensor.shared value alongside PyMC random variables and use it directly inside a model. If you swap the saturation function, every downstream computation updates automatically.

sat = MichaelisMentenSaturation()

def saturation_derivative(x, alpha, lam):

"""Auto-diff derivative of the saturation function.

x can be a pt.dvector (plotting), or a pytensor.shared (PyMC models).

alpha, lam can be symbolic variables or PyMC random variables.

"""

f = sat.function(x, alpha, lam)

return pt.grad(f.sum(), x)

# Compiled function for numerical evaluation (plotting)

_x_v = pt.dvector("x")

_alpha_s = pt.dscalar("alpha")

_lam_s = pt.dscalar("lam")

derivative_michaelis_menten = pytensor_function(

[_x_v, _alpha_s, _lam_s],

saturation_derivative(_x_v, _alpha_s, _lam_s),

)

x_test = np.array([0.5, 1.0, 2.0, 4.0])

derivs = derivative_michaelis_menten(x_test, 2.75, 2.50)

pd.DataFrame({"x": x_test, "f'(x)": np.round(derivs, 4)}).head()| x | f'(x) | |

|---|---|---|

| 0 | 0.5 | 0.7639 |

| 1 | 1.0 | 0.5612 |

| 2 | 2.0 | 0.3395 |

| 3 | 4.0 | 0.1627 |

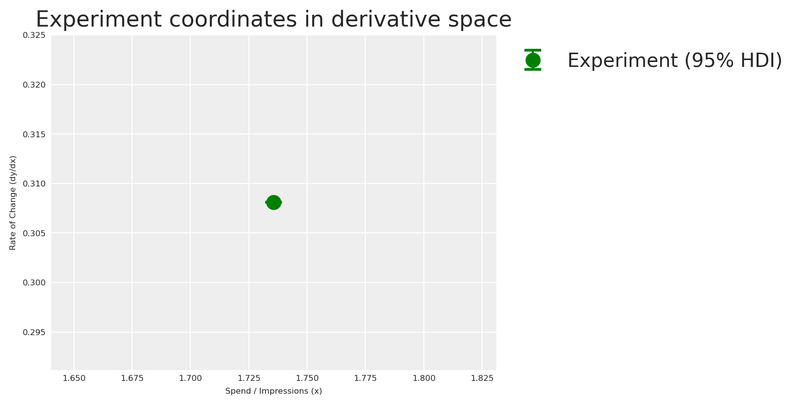

We have the total lost sales and the total lost spend over the treatment window. To place our experiment in the derivative space, we compute the average rate of change — total sales impact divided by total spend reduction — and evaluate it at the midpoint between the counterfactual and actual spend levels.

Theoretical nuance: Secant vs Tangent

This is an approximation based on the Mean Value Theorem. Because the Michaelis-Menten curve is concave, the slope of the secant line (average rate of change over the spend drop) is only an approximation of the instantaneous tangent line (f'(x)) at the exact midpoint. Additionally, measuring sales drops over a fixed time window means we might not capture the full steady-state drop if adstock (carryover) effects are long-lasting. For our purposes, it serves as an excellent anchor, but it’s important to recognize the underlying mechanics.

Raw spend vs adstocked spend

The experimental \Delta X is computed from raw media spend, but the MMM’s saturation function operates on adstocked spend — the signal after geometric decay has been applied. This means the coordinate system of our experimental observation (raw-spend units) does not perfectly align with the coordinate system of the saturation curve (adstocked-spend units).

This approximation is most sustainable when the adstock effect is mild (low decay parameter \alpha), because the adstocked signal stays close to the raw signal. Under heavy adstock (high \alpha, long l_{\text{max}}), the transformation can meaningfully compress and shift the spend distribution, making the raw-spend midpoint a less accurate anchor. The approach remains directionally valid — the experiment still provides genuine causal information about the saturation regime — but practitioners should be aware that the alignment degrades as carryover effects grow stronger.

Code

# Full posterior of rate of change

rate_of_change_samples = np.abs(total_effect_samples) / total_delta_spend

average_rate_of_change = rate_of_change_samples.mean()

rate_of_change_std = rate_of_change_samples.std()

# HDI directly from the rate-of-change posterior

rate_hdi = az.hdi(rate_of_change_samples, hdi_prob=0.95)

rate_of_change_lower, rate_of_change_upper = rate_hdi

# Midpoint of the two spend levels (counterfactual vs actual)

x_midpoint = (counterfactual_spend_per_week + actual_spend_per_week) / 2

pd.DataFrame({

"Average rate of change (dy/dx)": [round(average_rate_of_change, 4)],

"Std": [round(rate_of_change_std, 4)],

"95% HDI lower": [round(rate_of_change_lower, 4)],

"95% HDI upper": [round(rate_of_change_upper, 4)],

"X midpoint": [round(x_midpoint, 4)],

}).head()

fig, ax = plt.subplots()

yerr_low = max(0, average_rate_of_change - rate_of_change_lower)

yerr_high = max(0, rate_of_change_upper - average_rate_of_change)

ax.errorbar(

x_midpoint, average_rate_of_change,

yerr=[[yerr_low], [yerr_high]],

fmt="o", color="green", capsize=6, capthick=2, markersize=10, zorder=5,

label="Experiment (95% HDI)",

)

ax.set(

xlabel="Spend / Impressions (x)",

ylabel="Rate of Change (dy/dx)",

title="Experiment coordinates in derivative space",

)

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

Now that we have our experimental observation in derivative space, we can estimate the saturation parameters \alpha and \lambda that are consistent with this evidence.

The Identification Problem

Mathematically, a single point in derivative space cannot uniquely identify a two-parameter curve (\alpha and \lambda). There is an infinite family of curves that can pass through this exact rate of change at this exact spend level. A point optimizer would return just one of them and discard all that degeneracy. By using a Bayesian model instead, the posterior naturally captures the full landscape of plausible (\alpha, \lambda) combinations — including the correlation between them. This is exactly why we fit a small PyMC model here rather than use a point optimizer.

We build a small PyMC model whose likelihood matches our experimental observation. The priors are weakly informative half-normals — positive but agnostic — so the experimental observation drives the posterior. The model says: “the derivative of Michaelis-Menten at our spend midpoint, evaluated with unknown \alpha and \lambda, should produce the rate of change we observed, with noise equal to the experimental standard deviation.”

Code

x_range = np.linspace(0, 8, 200)

with pm.Model() as prior_elicitation_model:

cal_alpha = pm.HalfNormal("cal_alpha", sigma=3)

cal_lam = pm.HalfNormal("cal_lam", sigma=3)

x_pt = pytensor.shared(np.float64(x_midpoint), name="x_eval")

predicted_rate = saturation_derivative(x_pt, cal_alpha, cal_lam)

pm.Normal(

"obs",

mu=predicted_rate,

sigma=rate_of_change_std,

observed=average_rate_of_change,

)

elicitation_idata = pm.sample(

draws=250,

random_seed=seed,

target_accept=0.95,

)

elic_alpha_posterior = elicitation_idata.posterior["cal_alpha"].values.flatten()

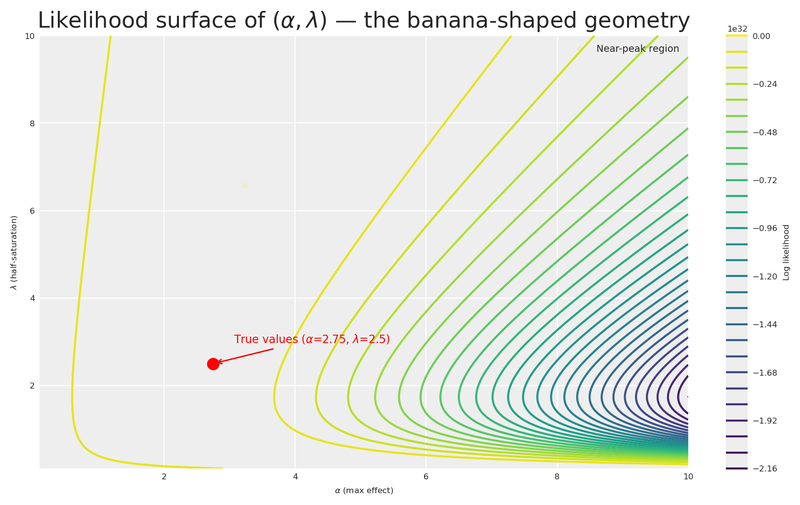

elic_lam_posterior = elicitation_idata.posterior["cal_lam"].values.flatten()As expected from the identification problem above, the joint posterior of (\alpha, \lambda) exhibits strong correlation. To expose this geometry clearly, we borrow a technique from Daniel Saunders’ excellent Geometric Intuition for Media Mix Models: we evaluate the log-likelihood on a 2D grid and plot contour lines — revealing the characteristic banana-shaped surface.

Code

alphas_grid = np.linspace(0.1, 10, 200)

lams_grid = np.linspace(0.1, 10, 200)

A_grid, L_grid = np.meshgrid(alphas_grid, lams_grid)

deriv_on_grid = (A_grid * L_grid) / (L_grid + x_midpoint) ** 2

log_lik_surface = sp_stats.norm(

loc=deriv_on_grid, scale=rate_of_change_std

).logpdf(average_rate_of_change)

lik_peak = np.nanmax(log_lik_surface)

near_lik_mask = log_lik_surface >= lik_peak - 1.5

a_near_lik = A_grid[near_lik_mask]

l_near_lik = L_grid[near_lik_mask]

fig, ax = plt.subplots(figsize=(8, 5))

contour = ax.contour(A_grid, L_grid, log_lik_surface, levels=30)

ax.plot(

a_near_lik, l_near_lik, "o",

color="gold", alpha=0.12, markersize=3,

label="Near-peak region",

)

ax.plot(TRUE_ALPHA_META, TRUE_LAM_META, "o", color="red", markersize=8, zorder=10)

ax.annotate(

rf"True values ($\alpha$={TRUE_ALPHA_META}, $\lambda$={TRUE_LAM_META})",

(TRUE_ALPHA_META, TRUE_LAM_META),

xytext=(15, 15), textcoords="offset points", fontsize=8,

arrowprops=dict(arrowstyle="->", color="red"), color="red",

)

plt.colorbar(contour, ax=ax, label="Log likelihood")

ax.set(

xlabel=r"$\alpha$ (max effect)",

ylabel=r"$\lambda$ (half-saturation)",

title=r"Likelihood surface of $(\alpha, \lambda)$ — the banana-shaped geometry",

)

ax.legend(loc="upper right", fontsize=7)

plt.show()

The contour plot reveals the characteristic banana-shaped geometry that Daniel Saunders describes so well: there is an extended region of nearly equivalent likelihood where high \alpha paired with high \lambda produces a similar derivative to low \alpha paired with low \lambda. The gold markers highlight a wide corridor of plausible parameter combinations that the data alone cannot distinguish.

This is precisely the insight Daniel drives home: it is not the amount of data that resolves the banana, but how well the data is distributed across the saturation curve. A single experiment at one spend level leaves us with this long ridge of near-equivalent solutions. Gentle, informed priors are what trim the implausible tails — let’s build them.

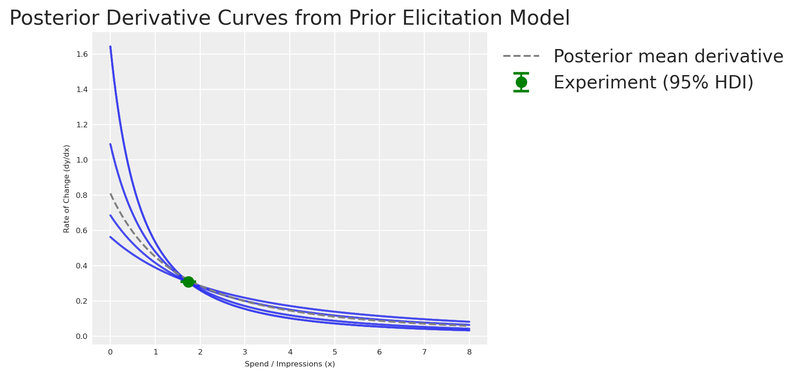

Let’s now visualise the posterior distribution of derivative curves against the experimental observation!

Code

fig, ax = plt.subplots()

# Posterior fan: sample 200 curves from the joint posterior

n_curves = 200

idx = rng.choice(len(elic_alpha_posterior), n_curves, replace=False)

for i in idx:

y_curve = derivative_michaelis_menten(x_range, elic_alpha_posterior[i], elic_lam_posterior[i])

ax.plot(x_range, y_curve, color="C0", alpha=0.03)

# Posterior mean curve

mean_curve = derivative_michaelis_menten(

x_range, elic_alpha_posterior.mean(), elic_lam_posterior.mean()

)

ax.plot(x_range, mean_curve, label="Posterior mean derivative", color="grey", linestyle="--")

ax.errorbar(

x_midpoint, average_rate_of_change,

yerr=[[yerr_low], [yerr_high]],

fmt="o", color="green", capsize=6, capthick=2, markersize=8, zorder=5,

label="Experiment (95% HDI)",

)

ax.set(

xlabel="Spend / Impressions (x)",

ylabel="Rate of Change (dy/dx)",

title="Posterior Derivative Curves from Prior Elicitation Model",

)

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

With the elicitation posterior in hand, let’s feed this knowledge into our MMM.

The generic MMM

First, let’s see what happens when we build a model with default priors — no experimental knowledge injected. This is our baseline: the naive approach.

X = df[["ds", "meta", "google", "trend"]].copy()

y = df["venezuela"].copy()We create the model using the multidimensional MMM class from pymc-marketing. Even though we have a single market here (no dims parameter), the class from pymc_marketing.mmm.multidimensional is the unified entry point for all MMM models.

adstock_generic = GeometricAdstock(

priors={"alpha": Prior("Beta", alpha=2, beta=5, dims="channel")},

l_max=4,

)

saturation_generic = MichaelisMentenSaturation(

priors={

"alpha": Prior("HalfNormal", sigma=1, dims="channel"),

"lam": Prior("Gamma", mu=2, sigma=1, dims="channel"),

},

)

generic_mmm = MMM(

date_column="ds",

target_column="venezuela",

channel_columns=["meta", "google"],

control_columns=["trend"],

adstock=adstock_generic,

saturation=saturation_generic,

yearly_seasonality=4,

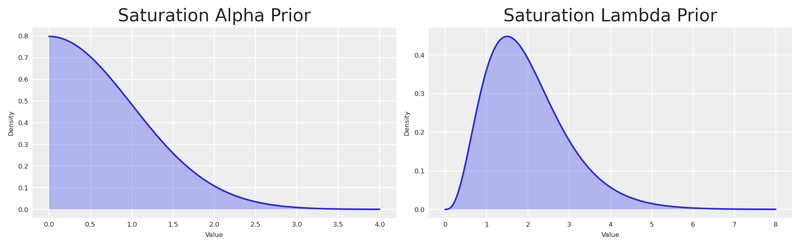

)Let’s examine the default priors and visualise them with PreliZ.

Code

prior_alpha = pz.HalfNormal(sigma=1)

prior_lam = pz.Gamma(mu=2, sigma=1)

fig, axes = plt.subplots(nrows=1, ncols=2, figsize=(10, 3))

# Plot Alpha Prior manually

x_alpha = np.linspace(0, 4, 1000)

y_alpha = prior_alpha.pdf(x_alpha)

axes[0].plot(x_alpha, y_alpha)

axes[0].fill_between(x_alpha, y_alpha, alpha=0.3)

axes[0].set(title="Saturation Alpha Prior", xlabel="Value", ylabel="Density")

# Plot Lambda Prior manually

x_lam = np.linspace(0, 8, 1000)

y_lam = prior_lam.pdf(x_lam)

axes[1].plot(x_lam, y_lam)

axes[1].fill_between(x_lam, y_lam, alpha=0.3)

axes[1].set(title="Saturation Lambda Prior", xlabel="Value", ylabel="Density")

plt.show()

Note

By using Gamma and HalfNormal priors we impose structure — constraining these parameters to be positive. But the distributions are quite wide. Let’s see how their mean compares to our experiment.

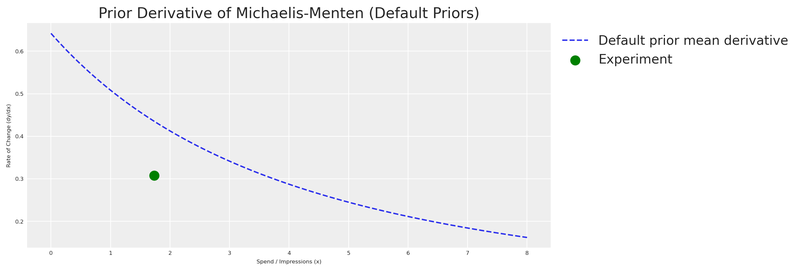

We sample from the prior and visualise the derivative of the Michaelis-Menten function implied by those default priors.

Code

generic_mmm.build_model(X, y)

with generic_mmm.model:

prior_predictive = pm.sample_prior_predictive(

random_seed=seed,

var_names=["saturation_alpha", "saturation_lam"],

)

prior_alpha_mean = prior_predictive.prior["saturation_alpha"].mean().item()

prior_lambda_mean = prior_predictive.prior["saturation_lam"].mean().item()

x_values = np.linspace(0, 8, 500)

prior_mm_mean_derivative = derivative_michaelis_menten(

x_values,

prior_alpha_mean * df.venezuela.max(),

prior_lambda_mean * df.meta.max(),

)

fig, ax = plt.subplots(figsize=(12, 4))

ax.plot(

x_values, prior_mm_mean_derivative,

color="C0", label="Default prior mean derivative", linestyle="--",

)

ax.scatter(

x_midpoint, abs(average_rate_of_change),

color="green", label="Experiment", s=100, zorder=5,

)

ax.set(

xlabel="Spend / Impressions (x)",

ylabel="Rate of Change (dy/dx)",

title="Prior Derivative of Michaelis-Menten (Default Priors)",

)

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

As expected, the default prior derivative is far from our experiment. The model has no knowledge of the actual saturation behaviour — it’s working with a vague, uninformed guess. This is our motivation for eliciting experiment-informed priors.

The experiment-informed MMM

Now let’s turn the elicitation posterior into informative priors for the MMM. PyMC-Marketing internally scales the data using Max Abs Scaler. This means values are divided by their maximum. Since \alpha lives on the Y-axis (sales) and \lambda on the X-axis (spend), we scale the entire posterior accordingly, then extract the 95% HDI as the bounds for find_constrained_prior.

Code

y_max = df.venezuela.max()

x_max = df.meta.max()

# Scale the full posterior

scaled_alpha_samples = elic_alpha_posterior / y_max

scaled_lam_samples = elic_lam_posterior / x_max

# HDI of the scaled posteriors

scaled_alpha_hdi = az.hdi(scaled_alpha_samples, hdi_prob=0.95)

scaled_lam_hdi = az.hdi(scaled_lam_samples, hdi_prob=0.95)

scaled_alpha_lower, scaled_alpha_upper = scaled_alpha_hdi

scaled_lam_lower, scaled_lam_upper = scaled_lam_hdi

pd.DataFrame({

"Parameter": ["alpha (scaled)", "lambda (scaled)"],

"Mean": [round(scaled_alpha_samples.mean(), 4), round(scaled_lam_samples.mean(), 4)],

"95% HDI lower": [round(scaled_alpha_lower, 4), round(scaled_lam_lower, 4)],

"95% HDI upper": [round(scaled_alpha_upper, 4), round(scaled_lam_upper, 4)],

}).head()| Parameter | Mean | 95% HDI lower | 95% HDI upper | |

|---|---|---|---|---|

| 0 | alpha (scaled) | 0.3779 | 0.3409 | 0.4409 |

| 1 | lambda (scaled) | 0.7252 | 0.3269 | 1.2171 |

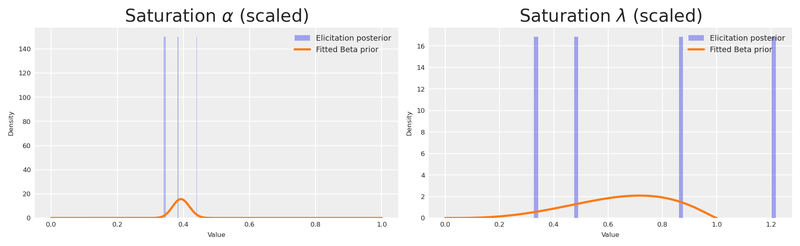

The scaled posterior values fall within [0, 1], making the Beta distribution a natural choice. We use PyMC’s find_constrained_prior to identify Beta parameters that concentrate 95% of their mass within the elicitation posterior’s HDI.

Posterior-as-prior: a fully Bayesian pipeline

The bounds we pass to find_constrained_prior come directly from the posterior of the elicitation model, which already captured experimental noise and the structural correlation between \alpha and \lambda. Every source of uncertainty flows naturally from experiment → elicitation model → MMM prior.

Code

alpha_custom_prior = pm.find_constrained_prior(

pm.Beta,

lower=max(scaled_alpha_lower, 0.01),

upper=min(scaled_alpha_upper, 0.99),

mass=0.95,

init_guess={"alpha": 2, "beta": 2},

)

lam_custom_prior = pm.find_constrained_prior(

pm.Beta,

lower=max(scaled_lam_lower, 0.01),

upper=min(scaled_lam_upper, 0.99),

mass=0.95,

init_guess={"alpha": 3, "beta": 3},

)

pd.DataFrame({

"Parameter": ["saturation_alpha", "saturation_lam"],

"Beta alpha": [round(alpha_custom_prior["alpha"], 4), round(lam_custom_prior["alpha"], 4)],

"Beta beta": [round(alpha_custom_prior["beta"], 4), round(lam_custom_prior["beta"], 4)],

}).head()| Parameter | Beta alpha | Beta beta | |

|---|---|---|---|

| 0 | saturation_alpha | 144.7220 | 223.4610 |

| 1 | saturation_lam | 4.0365 | 2.2068 |

Let’s verify that the fitted Beta distributions faithfully reproduce the elicitation posterior. We overlay the Beta PDF on a histogram of the scaled posterior samples — if the two agree, we can trust that the information transfer from experiment to MMM prior is faithful.

Code

custom_prior_alpha_dist = pz.Beta(**alpha_custom_prior)

custom_prior_lam_dist = pz.Beta(**lam_custom_prior)

fig, axes = plt.subplots(nrows=1, ncols=2, figsize=(10, 3))

x_beta = np.linspace(0, 1, 1000)

axes[0].hist(scaled_alpha_samples, bins=60, density=True, alpha=0.4, color="C0", label="Elicitation posterior")

axes[0].plot(x_beta, custom_prior_alpha_dist.pdf(x_beta), color="C1", lw=2, label="Fitted Beta prior")

axes[0].set(title=r"Saturation $\alpha$ (scaled)", xlabel="Value", ylabel="Density")

axes[0].legend(fontsize=7)

axes[1].hist(scaled_lam_samples, bins=60, density=True, alpha=0.4, color="C0", label="Elicitation posterior")

axes[1].plot(x_beta, custom_prior_lam_dist.pdf(x_beta), color="C1", lw=2, label="Fitted Beta prior")

axes[1].set(title=r"Saturation $\lambda$ (scaled)", xlabel="Value", ylabel="Density")

axes[1].legend(fontsize=7)

plt.show()

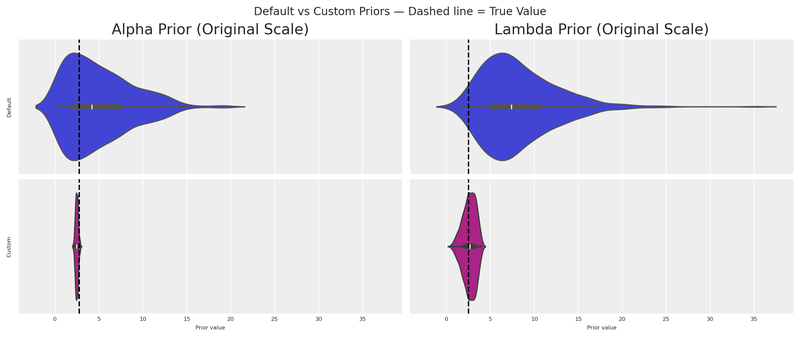

Let’s put the default and custom distributions side by side, in original scale, with the true values marked as vertical lines.

Code

n_samples = 500

# Default priors (original scale)

default_alpha_samples = prior_alpha.rvs(n_samples) * df.venezuela.max()

default_lam_samples = prior_lam.rvs(n_samples) * df.meta.max()

# Custom priors (original scale)

custom_alpha_samples = custom_prior_alpha_dist.rvs(n_samples) * df.venezuela.max()

custom_lam_samples = custom_prior_lam_dist.rvs(n_samples) * df.meta.max()

fig, axes = plt.subplots(nrows=2, ncols=2, figsize=(12, 5), sharex=True, sharey=True)

sns.violinplot(data=default_alpha_samples, color="C0", orient="h", ax=axes[0, 0])

sns.violinplot(data=default_lam_samples, color="C0", orient="h", ax=axes[0, 1])

sns.violinplot(data=custom_alpha_samples, color="C3", orient="h", ax=axes[1, 0])

sns.violinplot(data=custom_lam_samples, color="C3", orient="h", ax=axes[1, 1])

# True values

axes[0, 0].axvline(TRUE_ALPHA_META, color="black", linestyle="--")

axes[0, 1].axvline(TRUE_LAM_META, color="black", linestyle="--")

axes[1, 0].axvline(TRUE_ALPHA_META, color="black", linestyle="--")

axes[1, 1].axvline(TRUE_LAM_META, color="black", linestyle="--")

axes[0, 0].set(title="Alpha Prior (Original Scale)", ylabel="Default")

axes[0, 1].set(title="Lambda Prior (Original Scale)")

axes[1, 0].set(xlabel="Prior value", ylabel="Custom")

axes[1, 1].set(xlabel="Prior value")

fig.suptitle("Default vs Custom Priors — Dashed line = True Value", fontsize=12)

plt.show()

The custom distributions are dramatically more concentrated around the true values. Even with a single experiment, we’ve gained substantial information.

We pass the custom priors into the transformation objects. Note how we set a tight, experiment-informed prior for meta (the channel we experimented on) while keeping a wider prior for google (no experimental evidence yet).

adstock_informed = GeometricAdstock(

priors={"alpha": Prior("Beta", alpha=2, beta=5, dims="channel")},

l_max=4,

)

saturation_informed = MichaelisMentenSaturation(

priors={

"alpha": Prior(

"Beta",

alpha=np.array([alpha_custom_prior["alpha"], 1.8]),

beta=np.array([alpha_custom_prior["beta"], 2.0]),

dims="channel",

),

"lam": Prior(

"Beta",

alpha=np.array([lam_custom_prior["alpha"], 1.8]),

beta=np.array([lam_custom_prior["beta"], 2.0]),

dims="channel",

),

},

)

informed_mmm = MMM(

date_column="ds",

target_column="venezuela",

channel_columns=["meta", "google"],

control_columns=["trend"],

adstock=adstock_informed,

saturation=saturation_informed,

yearly_seasonality=4,

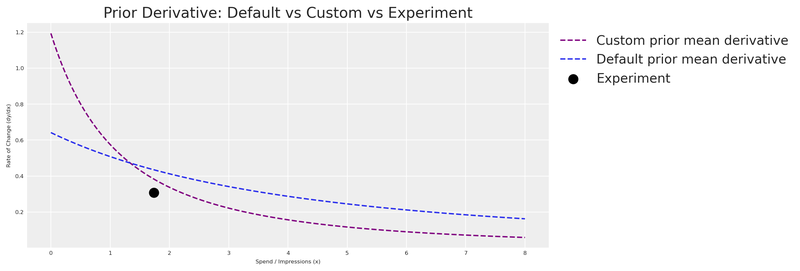

)Let’s visualise the derivative of the Michaelis-Menten function for both the default and custom priors, together with the experimental observation.

Code

informed_mmm.build_model(X, y)

with informed_mmm.model:

custom_prior_predictive = pm.sample_prior_predictive(

random_seed=seed,

var_names=["saturation_alpha", "saturation_lam"],

)

custom_prior_alpha_mean = custom_prior_predictive.prior["saturation_alpha"].mean().item()

custom_prior_lambda_mean = custom_prior_predictive.prior["saturation_lam"].mean().item()

custom_prior_mm_mean_derivative = derivative_michaelis_menten(

x_values,

custom_prior_alpha_mean * df.venezuela.max(),

custom_prior_lambda_mean * df.meta.max(),

)

fig, ax = plt.subplots(figsize=(12, 4))

ax.plot(

x_values, custom_prior_mm_mean_derivative,

color="purple", label="Custom prior mean derivative", linestyle="--",

)

ax.plot(

x_values, prior_mm_mean_derivative,

color="C0", label="Default prior mean derivative", linestyle="--",

)

ax.scatter(

x_midpoint, abs(average_rate_of_change),

color="black", label="Experiment", s=100, zorder=5,

)

ax.set(

xlabel="Spend / Impressions (x)",

ylabel="Rate of Change (dy/dx)",

title="Prior Derivative: Default vs Custom vs Experiment",

)

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

As expected, the custom prior derivative is much closer to our experimental observation. The model now enters MCMC sampling with a strong, evidence-based starting point.

With the priors in place, let’s fit the model.

Code

fit_kwargs = dict(

draws=250,

target_accept=0.95,

chains=4,

random_seed=rng,

)

idata = informed_mmm.fit(X=X, y=y, **fit_kwargs)Code

summary = az.summary(

idata,

var_names=["saturation_lam", "saturation_alpha"],

round_to=2,

)

summary.head(10)| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| saturation_lam[google] | 0.65 | 0.18 | 0.33 | 0.95 | 0.01 | 0.0 | 581.68 | 480.26 | 1.01 |

| saturation_lam[meta] | 0.67 | 0.15 | 0.41 | 0.94 | 0.01 | 0.0 | 465.20 | 487.24 | 1.01 |

| saturation_alpha[google] | 0.39 | 0.02 | 0.34 | 0.43 | 0.00 | 0.0 | 784.39 | 820.47 | 1.00 |

| saturation_alpha[meta] | 0.45 | 0.04 | 0.39 | 0.52 | 0.00 | 0.0 | 523.37 | 603.93 | 1.01 |

Let’s compare the posterior estimates against the true values we embedded in the DGP.

Code

posterior_alpha_meta = (

informed_mmm.idata.posterior["saturation_alpha"]

.sel(channel="meta")

.mean()

.item() * df.venezuela.max()

)

posterior_lam_meta = (

informed_mmm.idata.posterior["saturation_lam"]

.sel(channel="meta")

.mean()

.item() * df.meta.max()

)

pd.DataFrame({

"Parameter": ["alpha (meta)", "lambda (meta)"],

"Posterior mean": [round(posterior_alpha_meta, 2), round(posterior_lam_meta, 2)],

"True value": [TRUE_ALPHA_META, TRUE_LAM_META],

}).head()| Parameter | Posterior mean | True value | |

|---|---|---|---|

| 0 | alpha (meta) | 2.85 | 2.75 |

| 1 | lambda (meta) | 2.73 | 2.50 |

The experiment-informed model recovers parameter values much closer to the ground truth for meta — the channel we ran the experiment on. For google, the wider prior means the model relies more on the data to learn the parameters, which is exactly the intended behaviour.

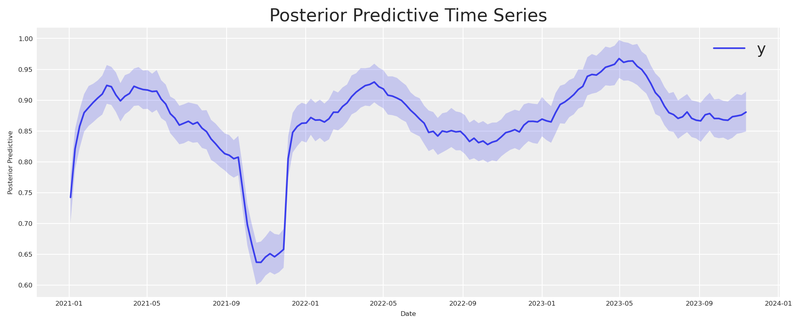

Finally, let’s verify the model fit with a posterior predictive check.

Code

informed_mmm.sample_posterior_predictive(X=X, extend_idata=True, random_seed=seed)

informed_mmm.plot.posterior_predictive()

plt.show()

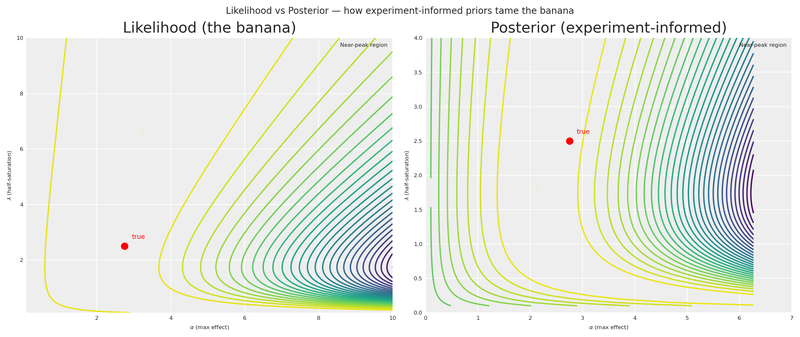

The banana, tamed

We started with a banana-shaped likelihood surface — a long corridor of parameter combinations that the experiment alone could not distinguish. Now that the full pipeline is in place (experiment → elicitation → Beta priors → MMM), let’s return to that surface and see what the informed priors buy us.

Following the decomposition approach in William B. Dean’s interactive Marimo adaptation of Daniel Saunders’ geometric intuition post, we place the Likelihood and Posterior side by side on the same axes. The likelihood is unchanged — same banana as before. The posterior adds the experiment-informed Beta priors we derived from the elicitation model.

Code

scaled_A = A_grid / df.venezuela.max()

scaled_L = L_grid / df.meta.max()

valid_mask = (scaled_A > 0) & (scaled_A < 1) & (scaled_L > 0) & (scaled_L < 1)

log_informed_prior = np.full_like(A_grid, -np.inf)

log_informed_prior[valid_mask] = (

sp_stats.beta(

alpha_custom_prior["alpha"], alpha_custom_prior["beta"]

).logpdf(scaled_A[valid_mask])

+ sp_stats.beta(

lam_custom_prior["alpha"], lam_custom_prior["beta"]

).logpdf(scaled_L[valid_mask])

)

log_informed_posterior = log_lik_surface + log_informed_prior

post_peak = np.nanmax(log_informed_posterior)

near_post_mask = log_informed_posterior >= post_peak - 1.5

a_near_post = A_grid[near_post_mask]

l_near_post = L_grid[near_post_mask]

def _plot_surface(surface, ax, title, show_ylabel=True):

c = ax.contour(A_grid, L_grid, surface, levels=30)

ax.plot(TRUE_ALPHA_META, TRUE_LAM_META, "o", color="red", markersize=7, zorder=10)

ax.annotate(

"true", (TRUE_ALPHA_META, TRUE_LAM_META),

xytext=(8, 8), textcoords="offset points", fontsize=7, color="red",

)

ax.set(xlabel=r"$\alpha$ (max effect)", title=title)

if show_ylabel:

ax.set_ylabel(r"$\lambda$ (half-saturation)")

return c

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

_plot_surface(log_lik_surface, axes[0], "Likelihood (the banana)")

axes[0].plot(

a_near_lik, l_near_lik, "o",

color="gold", alpha=0.12, markersize=2,

label="Near-peak region",

)

axes[0].legend(loc="upper right", fontsize=6)

_plot_surface(

log_informed_posterior, axes[1],

"Posterior (experiment-informed)",

)

axes[1].plot(

a_near_post, l_near_post, "o",

color="gold", alpha=0.12, markersize=2,

label="Near-peak region",

)

axes[1].legend(loc="upper right", fontsize=6)

axes[1].set(xlim=(0, 7), ylim=(0, 4))

fig.suptitle(

r"Likelihood vs Posterior — how experiment-informed priors tame the banana",

fontsize=10,

)

plt.show()

The contrast is striking. The Likelihood panel shows the same untamed banana we saw earlier — a wide ridge of near-equivalent solutions stretching from low \alpha/low \lambda all the way to the upper-right corner. The Posterior panel shows how the experiment-informed Beta priors concentrate the mass around the true values, collapsing that corridor into a compact region. The gold markers on each panel make the difference visceral: the informed posterior’s near-peak region is a fraction of the likelihood’s.

This is the payoff of the entire pipeline. A single experiment, translated through derivative space into a Bayesian elicitation model and then into Beta priors, transforms a nearly unidentifiable surface into one that tightly brackets reality.

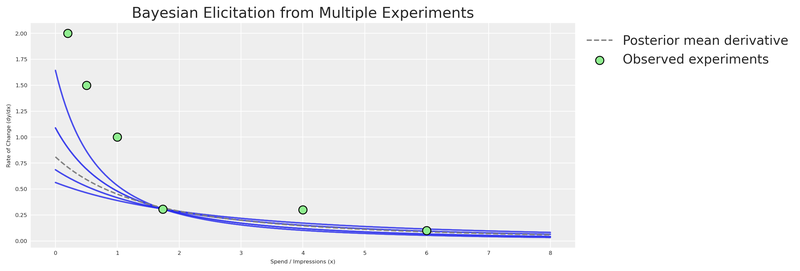

Tighter priors from multiple experiments

With a single experimental point, there are infinitely many curves that can fit it. If you have results from multiple experiments (different channels, different periods, different spend levels), you can combine them for a much more constrained elicitation.

Code

x_range_bonus = np.linspace(0, 8, 200)

multi_experiment_data = np.array([

(x_midpoint, average_rate_of_change, rate_of_change_std),

(1.0, 1.0, 0.15),

(0.5, 1.5, 0.20),

(4.0, 0.3, 0.08),

(6.0, 0.1, 0.05),

(0.2, 2.0, 0.25),

])

x_obs_multi = multi_experiment_data[:, 0]

y_obs_multi = multi_experiment_data[:, 1]

sigma_obs_multi = multi_experiment_data[:, 2]

with pm.Model() as multi_elicitation_model:

cal_alpha_m = pm.HalfNormal("cal_alpha", sigma=3)

cal_lam_m = pm.HalfNormal("cal_lam", sigma=3)

x_pt_multi = pytensor.shared(x_obs_multi.astype(np.float64), name="x_obs")

predicted_rates = saturation_derivative(x_pt_multi, cal_alpha_m, cal_lam_m)

pm.Normal(

"obs",

mu=predicted_rates,

sigma=sigma_obs_multi,

observed=y_obs_multi,

)

multi_idata = pm.sample(draws=250, random_seed=seed, target_accept=0.95)

multi_alpha_post = multi_idata.posterior["cal_alpha"].values.flatten()

multi_lam_post = multi_idata.posterior["cal_lam"].values.flatten()

n_curves_multi = 200

idx_multi = rng.choice(len(multi_alpha_post), n_curves_multi, replace=False)

fig, ax = plt.subplots(figsize=(12, 4))

for i in idx_multi:

y_curve = derivative_michaelis_menten(x_range_bonus, multi_alpha_post[i], multi_lam_post[i])

ax.plot(x_range_bonus, y_curve, color="C0", alpha=0.03)

mean_curve_multi = derivative_michaelis_menten(

x_range_bonus, multi_alpha_post.mean(), multi_lam_post.mean()

)

ax.plot(x_range_bonus, mean_curve_multi, label="Posterior mean derivative", color="grey", linestyle="--")

ax.scatter(

x_obs_multi, y_obs_multi,

label="Observed experiments",

color="lightgreen",

edgecolors="black",

s=80,

zorder=5,

)

ax.set(

xlabel="Spend / Impressions (x)",

ylabel="Rate of Change (dy/dx)",

title="Bayesian Elicitation from Multiple Experiments",

)

ax.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

More experiments = tighter elicitation = sharper priors = more accurate MMM. This is the virtuous cycle of combining experimentation with Bayesian modeling.

Considerations

Prior elicitation from experiments is a powerful tool, but it requires careful thought to implement correctly. Here are some key aspects to keep in mind.

Time variation matters. Every experiment is inherently connected to the time in which it was executed. Our MMM (as configured here) does not explicitly model time-varying media effects. Therefore, the contribution estimate is an average. After running multiple experiments across different periods, the average contribution detected in total should align with the model. But a single experiment may not. The nature of time variation was simplified in this example; in real life, it should be considered.

Tip

The multidimensional MMM supports time_varying_media=True for models that need to capture evolving channel effectiveness. This can help reconcile temporal differences between experiments and model estimates.

Organizational alignment. Beyond the mathematics, prior elicitation from experiments serves a crucial organizational function: it aligns the Experimentation and MMM teams. Often, these teams operate in silos, producing conflicting numbers that confuse leadership. By formally incorporating experimental results as priors in the MMM, you create a unified “source of truth” that respects both methodologies. This “peace treaty” is often as valuable as the accuracy gain itself.

Open source power. One of the greatest advantages of PyMC-Marketing and CausalPy is that they’re part of an open-source ecosystem. Unlike proprietary tools, these libraries can be combined, extended, and inspected:

- Build on existing work — leverage community intelligence.

- Create custom workflows — combine causal inference and Bayesian modeling in ways no single tool supports.

- Ensure transparency — methodologies are open for inspection and validation.

- Extend functionality — contribute to the codebase or build complementary tools.

We’ve shown how combining Bayesian modeling with causal inference creates a more robust approach to marketing measurement. This kind of integration would be very difficult with closed-source tools.

Conclusions

Quasi-experiments are a natural source of prior information. Using CausalPy’s

SyntheticControl, we estimated the causal effect of reducing advertising spend — and translated that estimate into actionable prior distributions.The derivative of the saturation function is the bridge. By placing our experimental observation in derivative space, we connect real-world causal evidence to the parameters (\alpha, \lambda) of the saturation curve.

A small PyMC prior elicitation model replaces point optimization. The Bayesian elicitation model produces a full joint posterior that honestly represents what the experiment tells us — and multiple experiments pin down the curve further. Run experiments across different spend levels and time periods for the strongest elicitation.

Even a single experiment dramatically improves priors. The experiment-informed model’s priors were far more concentrated around the true values than the generic defaults, giving MCMC a much better starting point.

The multidimensional MMM from

pymc-marketingmakes this seamless. ThePriorclass, transformation objects (GeometricAdstock,MichaelisMentenSaturation), and the unifiedMMMclass let us inject experimental knowledge directly into the model specification — no hacks required.

Now it’s your turn to put this into practice. Run an experiment, extract the causal effect, build a prior elicitation model, and let your Bayesian MMM learn from evidence.

Recommended readings:

- Geometric Intuition for Media Mix Models — Daniel Saunders

- Causal Inference for the Brave and True

- What if? Causal inference through counterfactual reasoning in PyMC

- Causal analysis with PyMC: Answering “What If?” with the new do operator

- PyMC-Marketing: Lift Test Calibration (likelihood-based approach)

- Media Mix Model Calibration With Bayesian Priors — Zhang et al., Google Research (2024)

- Media Mix Model and Experimental Calibration: A Simulation Study — Juan Orduz

- PyMC-Marketing documentation

- CausalPy documentation

Version information

Code

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc_marketing,pytensorLast updated: Sat Feb 21 2026

Python implementation: CPython

Python version : 3.11.8

IPython version : 8.30.0

pymc_marketing: 0.17.1

pytensor : 2.37.0

numpy : 2.1.3

causalpy : 0.7.0

pymc_marketing: 0.17.1

matplotlib : 3.10.1

pymc_extras : 0.4.0

pandas : 2.2.3

arviz : 0.21.0

pymc : 5.27.1

seaborn : 0.13.2

pytensor : 2.37.0

scipy : 1.15.2

preliz : 0.20.0

Watermark: 2.5.0