import warnings

warnings.filterwarnings("ignore")

from pymc_marketing.mmm.budget_optimizer import BudgetOptimizer, BuildMergedModel, CustomModelWrapper

import pymc as pm

import arviz as az

import preliz as pz

import pytensor.tensor as pt

from pytensor import function as pytensor_function

# Visualization

import matplotlib.pyplot as plt

import seaborn as sns

# Scientific computing

import numpy as np

import pandas as pdDecision-Making Under Contradictions: Robust Budget Allocation When Your Models Disagree

MMM

python

decision theory

optimization

bayesian

pymc

marketing

robust optimization

How to make robust budget allocation decisions when your measurement models (MMM, experiments, attribution) give contradictory advice.

Introduction

You’re sitting in the quarterly business review. Finance asks a deceptively simple question: “Should we increase or decrease search spend next quarter?”

You look at your measurement systems. The regression model says search is a star — high incremental return, pour more money in. A recent experiment says social outperformed search by 3x during last month’s geo-test. Meanwhile, the attribution dashboard reports that display drives more contacts per dollar than any other channel.

Three systems. Three methodologies. Three contradictory numbers.

Finance doesn’t care about your methodological nuance. They need one decision. Increase or decrease? By how much? Across which channels?

This is the reality of modern marketing measurement. We don’t have one source of truth — we have multiple, competing views of how marketing works. Each view captures something real, but none tells the whole story. And the worst thing you can do is pretend this disagreement doesn’t exist.

How do you make a single, defensible budget decision when your models fundamentally disagree? Today we’ll answer that question. We’ll borrow a powerful idea from decision theory and robust optimization — minimax regret — and show how to find budget allocations that are robust to model error, regardless of which view turns out to be correct.

Quick summary

This article walks you through:

- Building three competing models of marketing effectiveness, each representing a different measurement philosophy (regression, experimentation, attribution).

- Showing that these models produce contradictory budget recommendations when optimised individually.

- Demonstrating why averaging or picking the most certain model are flawed strategies — including a dimensional analysis argument and a sensitivity test that makes the failure undeniable.

- Introducing minimax regret from classical decision theory as the principled resolution.

- Computing the normalised regret matrix and finding the robust allocation that minimizes worst-case regret as a fraction of optimal value.

- Connecting everything back to the PyMC-Marketing

BudgetOptimizer,BuildMergedModel, andCustomModelWrapper.

Three Views of Reality

Before we write a single line of code, let’s understand why these numbers disagree. Each measurement system answers a subtly different question:

| System | What it measures | Units (conceptual) | Typical uncertainty |

|---|---|---|---|

| Regression (MMM) | Average incremental contribution of marketing across time | Incremental sales per unit spend, averaged over the observation window | Moderate — many data points, but confounders and model misspecification add noise |

| Experiment | Incremental lift during a specific controlled period, not necessarily representative of average across larger periods | Incremental conversions per unit spend, holding everything else fixed | Moderate — randomisation or quasi-experimental design controls for confounders but validity depends on the assumptions being met |

| Attribution | Contacts or conversions attributed to marketing by the platform | Attributed contacts per unit spend — not necessarily incremental | Variable — high precision for what it measures, but what it measures may not be causal |

These three numbers don’t share the same dimensions. The regression model gives you an average marginal effect across time. The experiment gives you a point-in-time causal effect under specific conditions. The attribution model gives you a non-causal association because intention changes can’t be tracked by user level identifiers.

Key insight

You can’t simply average these numbers any more than you can average metres, kilograms, and seconds. They measure different things. But you still need to make a decision.

This is where decision theory enters the picture. But first, let’s make this concrete with code.

Modeling the disagreement

Let’s set up our environment and define the basic parameters for our models.

Code

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [8, 4]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["axes.labelsize"] = 6

plt.rcParams["xtick.labelsize"] = 6

plt.rcParams["ytick.labelsize"] = 6

plt.rcParams.update({"figure.constrained_layout.use": True})

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"

seed: int = sum(map(ord, "decision making under contradictions"))

rng: np.random.Generator = np.random.default_rng(seed=seed)

# print(f"Seed: {seed}")We’ll construct three PyMC models, each representing a different measurement system’s beliefs about channel effectiveness. All three models share the same structure — a Michaelis-Menten saturation curve per channel — but differ in their parameter values and uncertainty levels.

Assumption

We always have an assumption around our system, which should be share by the measurement tool used to estimate it. If we believe attribution is the real source of truth, and our system suffers from diminishing returns, then we should be able to observe the saturation curve in the attribution data. Same with an experiment, we should be able to observe the saturation curve in the experiment data, after we collect the data.

f(x) = \frac{\alpha \cdot x}{\lambda + x}

where:

- \alpha is the maximum achievable effect (the asymptote)

- \lambda is the half-saturation point (spend at which we reach half the maximum)

This function is concave, ensuring diminishing returns — a property that makes budget optimization both realistic and mathematically well-behaved. We’ll start by defining the global setup: three channels, our time horizon, and a total budget of 100.

Code

channels: list[str] = ["search", "social", "display"]

n_ch: int = len(channels)

# Observation periods (model structure) and future periods (optimization horizon)

n_dates: int = 30

n_future: int = 8

# Budget for optimization

TOTAL_BUDGET: float = 100.0

coords = {"date": np.arange(n_dates), "channel": channels}

# print(f"Channels: {channels}")

# print(f"Observation periods: {n_dates} | Future periods: {n_future}")

# print(f"Total budget: {TOTAL_BUDGET}")Here’s where the disagreement lives. Each measurement system has different beliefs about the saturation parameters (\alpha, \lambda) for each channel. Critically, they disagree about the channel ranking — and they disagree about the scale of marketing effectiveness.

Code

model_configs = {

"regression": {

"description": "MMM: average incrementality across time",

"mu_alpha": np.array([np.log(2.0), np.log(1.2), np.log(0.7)]),

"sigma_alpha": np.array([0.25, 0.25, 0.25]),

"mu_lam": np.array([np.log(5.0), np.log(3.0), np.log(4.0)]),

"sigma_lam": np.array([0.25, 0.25, 0.25]),

"color": "C0",

"ranking": "search > social > display",

},

"experiment": {

"description": "Experiment: causal lift in a specific period",

"mu_alpha": np.array([np.log(0.8), np.log(2.5), np.log(1.3)]),

"sigma_alpha": np.array([0.08, 0.08, 0.08]),

"mu_lam": np.array([np.log(6.0), np.log(3.0), np.log(3.5)]),

"sigma_lam": np.array([0.08, 0.08, 0.08]),

"color": "C1",

"ranking": "social > display > search",

},

"attribution": {

"description": "Attribution: contacts per dollar (not incremental — inflated scale)",

"mu_alpha": np.array([np.log(8.0), np.log(5.0), np.log(7.0)]),

"sigma_alpha": np.array([0.60, 0.60, 0.60]),

"mu_lam": np.array([np.log(2.5), np.log(7.0), np.log(3.0)]),

"sigma_lam": np.array([0.60, 0.60, 0.60]),

"color": "C2",

"ranking": "search > display > social",

},

}To turn these priors into something the optimiser can work with, we wrap each set of parameters in a lightweight PyMC model that speaks the same language as PyMC-Marketing’s CustomModelWrapper. The contract is simple: expose a channel_data matrix (budget per channel per date), a scalar total_contribution, and a vector channel_contribution.

Any version of reality can become a model

A common question is: “How do I actually turn my attribution dashboard (or any other measurement system) into a model like the ones above?” The answer is straightforward — you can take any version of reality and fit a model to it. Pick a response structure you believe in — say, one with saturation and adstock — and use your data to find the parameters that best replicate the behavior your measurement system reports. Attribution contacts per dollar, experimental lift curves, regression coefficients, even a colleague’s spreadsheet — any of these can serve as the “observed data” you fit against, with spend as the input.

The fitting itself can happen in two ways. A deterministic fit (e.g., least-squares or MLE) gives you point estimates of the parameters; you won’t get posteriors for free, but you can still estimate parameter uncertainty through confidence intervals or bootstrap. A Bayesian fit gives you full posteriors directly — plug them into an InferenceData object and you’re ready for the optimizer. Either route turns a measurement system into a model compatible with this framework.

One important nuance: fitting the same functional form to different data sources gives you models that are mathematically comparable — which is exactly what the minimax regret framework requires — but it does not make their outputs semantically equivalent. The attribution-fitted curve still represents attributed contacts, not causal lift. The models share a language, not a meaning. That’s precisely why we use regret within each model’s own terms rather than averaging across them.

We walk through a concrete example of this process — turning experimental results into calibrated model parameters — in From Experiments to Priors: Eliciting Informative Priors for Your Marketing Mix Model.

Code

def build_response_model(mu_alpha, sigma_alpha, mu_lam, sigma_lam, coords, n_dates, n_ch):

"""

Build a PyMC model with Michaelis-Menten saturation per channel.

Parameters

----------

mu_alpha : np.ndarray

LogNormal mu for saturation alpha (per channel).

sigma_alpha : np.ndarray

LogNormal sigma for saturation alpha (per channel).

mu_lam : np.ndarray

LogNormal mu for saturation lambda (per channel).

sigma_lam : np.ndarray

LogNormal sigma for saturation lambda (per channel).

coords : dict

PyMC coordinate dict with "date" and "channel".

n_dates : int

Number of observation periods.

n_ch : int

Number of channels.

Returns

-------

pm.Model

Compiled PyMC model.

"""

with pm.Model(coords=coords) as model:

# Channel spend data — the optimizer injects budget allocations here

channel_data = pm.Data(

"channel_data",

np.ones((n_dates, n_ch)),

dims=("date", "channel"),

)

# Saturation parameters (LogNormal ensures positivity)

alpha = pm.LogNormal(

"alpha",

mu=mu_alpha,

sigma=sigma_alpha,

dims="channel",

)

lam = pm.LogNormal(

"lam",

mu=mu_lam,

sigma=sigma_lam,

dims="channel",

)

# Michaelis-Menten saturation: alpha * x / (lam + x)

channel_contrib = alpha * channel_data / (lam + channel_data)

# Sum over channels → per-period response

mu = channel_contrib.sum(axis=-1)

# Deterministics the optimizer needs

pm.Deterministic("total_contribution", mu.sum())

pm.Deterministic(

"channel_contribution",

channel_contrib,

dims=("date", "channel"),

)

return model

# Build and sample all three models

models = {}

idatas = {}

for name, cfg in model_configs.items():

model = build_response_model(

mu_alpha=cfg["mu_alpha"],

sigma_alpha=cfg["sigma_alpha"],

mu_lam=cfg["mu_lam"],

sigma_lam=cfg["sigma_lam"],

coords=coords,

n_dates=n_dates,

n_ch=n_ch,

)

with model:

idata = pm.sample_prior_predictive(samples=500, random_seed=seed)

# Rename "prior" → "posterior" so the optimizer can find the parameter draws

idata.add_groups(posterior=idata.prior)

models[name] = model

idatas[name] = idata

# print(f"✓ {name}: posterior shape (alpha) = {idata.posterior['alpha'].shape}")We sample from the prior and treat those draws as if they were posterior samples from fitted models. In practice, each of these would come from a real analysis — the MMM from historical regression, the experiment from a geo-test, and the attribution from platform dashboards.

why use the prior as posterior?

By pretending the prior is the posterior, we skip the expensive MCMC step and focus on the decision-making problem. In a real workflow, these idata objects would come from pm.sample() after fitting your models to historical data. The downstream decision process is identical whether the posteriors come from real data or this synthetic generation.

Seeing the conflict

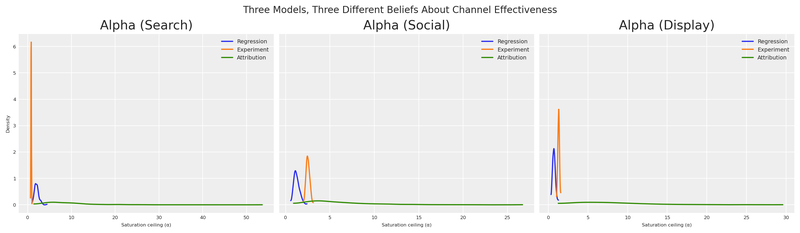

Let’s see how the three models differ in their beliefs about channel effectiveness (\alpha, the saturation ceiling). The width of each distribution reflects the measurement system’s certainty.

Code

fig, axes = plt.subplots(nrows=1, ncols=3, figsize=(14, 4), sharey=True)

for idx, ch in enumerate(channels):

ax = axes[idx]

for name, cfg in model_configs.items():

alpha_samples = idatas[name].posterior["alpha"].sel(channel=ch).values.flatten()

az.plot_dist(

alpha_samples,

color=cfg["color"],

label=name.capitalize(),

ax=ax,

)

ax.set(

title=f"Alpha ({ch.capitalize()})",

xlabel="Saturation ceiling (α)",

)

if idx == 0:

ax.set(ylabel="Density")

ax.legend(fontsize=7)

fig.suptitle(

"Three Models, Three Different Beliefs About Channel Effectiveness",

fontsize=12,

)

plt.show()

This plot is the visual proof of our predicament. These aren’t small disagreements — the models have qualitatively different channel rankings.

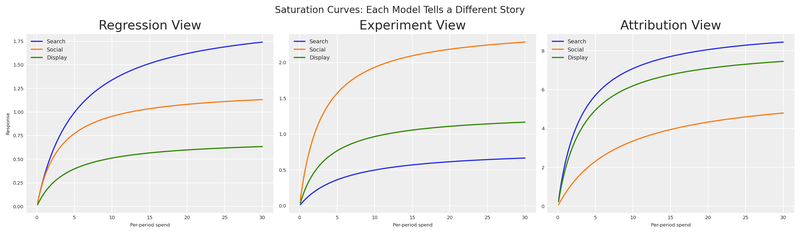

We can see this even more clearly by plotting the Michaelis-Menten response curves using each model’s posterior mean. This shows what each model predicts will happen as we increase spend on each channel.

Code

x_range = np.linspace(0.1, 30, 200)

fig, axes = plt.subplots(nrows=1, ncols=3, figsize=(14, 4), sharey=False)

for idx, (name, cfg) in enumerate(model_configs.items()):

ax = axes[idx]

for ch_idx, ch in enumerate(channels):

alpha_mean = idatas[name].posterior["alpha"].sel(channel=ch).mean().item()

lam_mean = idatas[name].posterior["lam"].sel(channel=ch).mean().item()

y = alpha_mean * x_range / (lam_mean + x_range)

ax.plot(x_range, y, label=ch.capitalize(), color=f"C{ch_idx}")

ax.set(

title=f"{name.capitalize()} View",

xlabel="Per-period spend",

ylabel="Response" if idx == 0 else "",

)

ax.legend(fontsize=7)

fig.suptitle("Saturation Curves: Each Model Tells a Different Story", fontsize=12)

plt.show()

Under the regression view, search (blue) dominates — it has the highest asymptote and responds well to increased spend. Under the experiment view, social (orange) is the runaway winner. Under the attribution view, search and display tower above social — but look at the y-axis: the attribution model reports effectiveness at a completely different scale than the other two. Its curves reach asymptotes 10× higher than anything regression or experiment predicts.

If you were a finance director looking at these three charts, you’d be understandably confused. And if someone averaged these curves, you’d be making a decision dominated by whichever system shouts the loudest numbers.

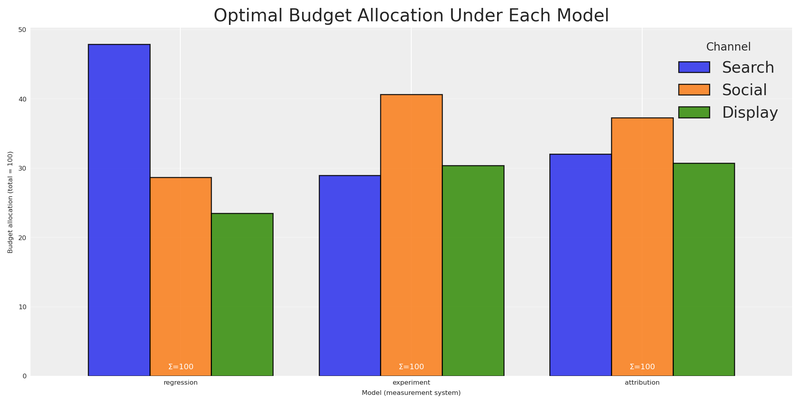

Three Models, Three Budgets

Let’s do what most teams do in practice: optimise budget allocation under each model independently, using the BudgetOptimizer from PyMC-Marketing. This gives us three separate optimal allocations, one for each belief system.

Code

bounds = {ch: (0.0, 60.0) for ch in channels}

optimal_allocations = {}

optimal_results = {}

for name in model_configs:

wrapper = CustomModelWrapper(

base_model=models[name],

idata=idatas[name],

channels=channels,

)

optimizer = BudgetOptimizer(model=wrapper, num_periods=n_future)

allocation, result = optimizer.allocate_budget(

total_budget=TOTAL_BUDGET,

budget_bounds=bounds,

)

# Convert to pd.Series for consistent downstream handling

if hasattr(allocation, "to_series"):

allocation = allocation.to_series()

elif not isinstance(allocation, pd.Series):

allocation = pd.Series(np.array(allocation).flatten(), index=channels)

optimal_allocations[name] = allocation

optimal_results[name] = result

# print(f"\n{name.upper()} optimal allocation:")

# print(f" Success: {result.success}")

# print(f" Expected contribution: {-result.fun:.4f}")

# for ch in channels:

# # print(f" {ch}: {allocation[ch]:.2f}")We can visualize these three optimal allocations to see exactly how the recommendations differ:

Code

alloc_df = pd.DataFrame(optimal_allocations).T

alloc_df.columns = [ch.capitalize() for ch in channels]

fig, ax = plt.subplots(figsize=(10, 5))

alloc_df.plot(kind="bar", ax=ax, edgecolor="black", alpha=0.85, width=0.8)

ax.set(

title="Optimal Budget Allocation Under Each Model",

xlabel="Model (measurement system)",

ylabel=f"Budget allocation (total = {TOTAL_BUDGET:.0f})",

)

ax.legend(title="Channel", loc="upper right")

ax.set_xticklabels(ax.get_xticklabels(), rotation=0)

# Annotate with total budget check

for i, name in enumerate(model_configs):

total = optimal_allocations[name].sum()

ax.text(i, 1, f"Σ={total:.0f}", ha="center", fontsize=7, color="white")

ax.grid(True, axis="y", alpha=0.3)

plt.show()

The picture is striking. The regression model puts the bulk of the budget into search. The experiment shifts almost everything to social. The attribution model favours search and display while starving social.

These aren’t minor tweaks — they are fundamentally different strategies. If you present any single one to finance, you’re implicitly betting that one measurement system is right and the others are wrong. How to decide? More importantly, what if you do it wrong? What if they’re all partially right?

The Illusion of Consensus

The natural instinct goes like this: “We have three models. Instead of trusting just one, let’s be smart — for any given allocation, we ask all three models what the expected outcome would be, then average their answers. This gives us a ‘consensus’ prediction. We optimise that.”

This sounds reasonable. It’s what a pragmatic stakeholder might actually propose. Let’s test it by merging all three models into a single computational graph using BuildMergedModel. This shared graph lets us evaluate any budget allocation across all three response surfaces simultaneously.

With the merged model ready, we can compile PyTensor evaluation functions to easily calculate the expected response for any budget under any model.

Code

wrappers = {

name: CustomModelWrapper(

base_model=models[name], idata=idatas[name], channels=channels,

)

for name in model_configs

}

merged = BuildMergedModel(

models=list(wrappers.values()),

prefixes=list(model_configs.keys()),

merge_on="channel_data",

)

merged.num_periods = n_future

merged.channel_columns = channels

# print("Merged model variables:")

# for v in merged.model.named_vars:

# # print(f" {v}")

merged_optimizer = BudgetOptimizer(

model=merged,

num_periods=n_future,

response_variable="regression_total_contribution",

)

eval_fns: dict[str, callable] = {}

draws_fns: dict[str, callable] = {}

for name in model_configs:

var = f"{name}_total_contribution"

dist = merged_optimizer.extract_response_distribution(var)

draws_fns[name] = pytensor_function([merged_optimizer._budgets_flat], dist)

eval_fns[name] = pytensor_function([merged_optimizer._budgets_flat], pt.mean(dist))

# Quick sanity check: evaluate at equal allocation

equal_alloc = np.array([TOTAL_BUDGET / n_ch] * n_ch)

# for name in model_configs:

# # print(f" {name} at equal alloc: {eval_fns[name](equal_alloc):.4f}")Now we build the “consensus” metric. For any allocation a, we evaluate all three models and average their expected responses:

V_{\text{avg}}(a) = \frac{1}{3}\left[V_{\text{reg}}(a) + V_{\text{exp}}(a) + V_{\text{attr}}(a)\right]

Then we optimise V_{\text{avg}} to find the allocation that maximizes this averaged prediction.

Code

with merged.model:

pm.Deterministic("averaged_total_contribution", (

merged.model["regression_total_contribution"]

+ merged.model["experiment_total_contribution"]

+ merged.model["attribution_total_contribution"]

) / 3)

avg_optimizer = BudgetOptimizer(

model=merged,

num_periods=n_future,

response_variable="averaged_total_contribution",

)

naive_avg, result_naive = avg_optimizer.allocate_budget(

total_budget=TOTAL_BUDGET,

budget_bounds=bounds,

)

if hasattr(naive_avg, "to_series"):

naive_avg = naive_avg.to_series()

elif not isinstance(naive_avg, pd.Series):

naive_avg = pd.Series(np.array(naive_avg).flatten(), index=channels)

# print(f"Optimisation success: {result_naive.success}")

# print(f"Averaged model expected contribution: {-result_naive.fun:.4f}")

# print(f"\nAveraged-model optimal allocation:")

# for ch in channels:

# # print(f" {ch}: {naive_avg[ch]:.2f}")

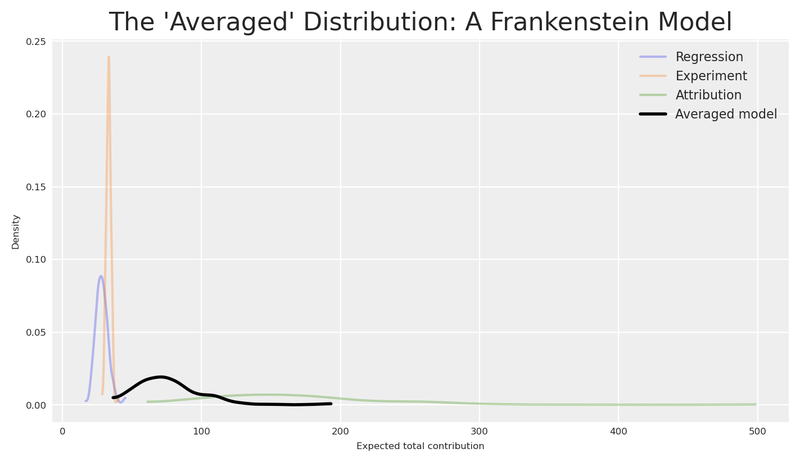

# print(f" Total: {naive_avg.sum():.2f}")This allocation is the best you can do if the average of all three models is meaningful. But is it?

Let’s look at what each model actually predicts for this allocation. Not just the mean — the full posterior distribution.

Code

fig, ax = plt.subplots(figsize=(7, 4))

alloc_values = naive_avg.values

all_draws = []

for name, cfg in model_configs.items():

draws = draws_fns[name](alloc_values)

all_draws.append(draws)

min_len = min(len(d) for d in all_draws)

stacked = np.column_stack([d[:min_len] for d in all_draws])

averaged_draws = stacked.mean(axis=1)

for name, cfg in model_configs.items():

draws = draws_fns[name](alloc_values)

az.plot_dist(draws, color=cfg["color"], label=name.capitalize(), ax=ax, plot_kwargs={"alpha": 0.3})

az.plot_dist(averaged_draws, color="black", label="Averaged model", ax=ax, plot_kwargs={"linewidth": 2})

ax.set(

title="The 'Averaged' Distribution: A Frankenstein Model",

xlabel="Expected total contribution",

ylabel="Density",

)

ax.legend(fontsize=8)

plt.show()

The distributions don’t just disagree — they live at completely different scales. The attribution model (green), operating at 10× the magnitude of the other two, pushes its distribution far to the right. Regression and experiment sit in a modest range; attribution towers above them. These aren’t minor calibration differences — they reflect fundamentally different measurement processes counting fundamentally different things.

The “averaged” distribution (black) doesn’t land in a neutral middle ground — it’s dragged toward the attribution model’s inflated values, because the average of a small number, another small number, and a very large number is dominated by the very large number. The loudest voice wins the average. Ask yourself: what does a draw from this distribution represent?

It’s not the expected incremental sales. It’s not the expected causal lift. It’s not the expected attributed contacts. It’s the average of all three — a quantity that exists in no framework.

The “consensus” approach takes the simple average of these three numbers. But think about what that means: we’re adding incremental sales on a set of point in time (or several points in time), causal conversions over a window of time, and attributed contacts not purely incremental as if they were the same thing. It’s like computing the average of 5 metres, 3 kilograms, and 7 seconds. The result is a number, sure — but it means nothing.

Additionally, the “consensus” implicitly assumes that the truth is exactly the arithmetic mean of the three models — giving 10× more weight to the system that happens to report the largest numbers. It doesn’t treat the models as equally credible hypotheses. It treats them as voting members of a committee where attribution gets ten votes and everyone else gets one.

Dimensional error

Averaging model outputs from different measurement systems is a dimensional error. The resulting “consensus” may look like a distribution, but it has no meaningful interpretation in any of the three frameworks. No draw from this distribution corresponds to any real-world outcome.

Even if we normalized everything to the same units (e.g., converted all to dollars), we’d still be averaging fundamentally different causal/non-causal quantities. Averaging these isn’t just a unit error; it’s a category error. It’s like averaging a speed (km/h), a distance (km), and a coordinate (lat/long). The dimensional analysis tells us averaging is conceptually broken. But how badly does it break in practice?

Why averaging fails at scale

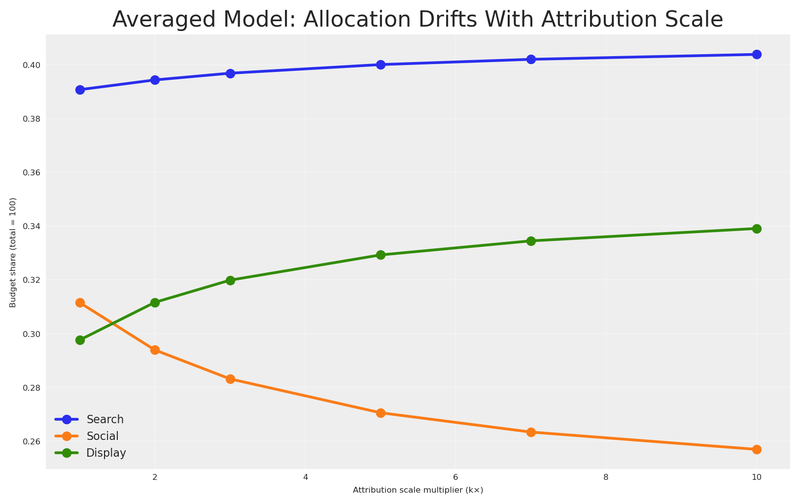

Let’s prove it. We’ll sweep the attribution model’s effectiveness parameter from its base value (1×) up to 10× — our current setting — and track what happens to both the averaged-model allocation and a robust alternative at each step. Regression and experiment stay fixed; only the attribution model’s magnitude changes.

If averaging is truly a sound strategy, the allocation it recommends should remain stable as one model’s scale changes. After all, a good aggregation method shouldn’t let a single voice dominate just because it speaks louder.

Code

# Base attribution alpha parameters (1× scale, before inflation)

base_mu_alpha_attr: np.ndarray = np.array([np.log(2.5), np.log(0.5), np.log(1.8)])

scale_factors: np.ndarray = np.array([1, 2, 3, 5, 7, 10])

n_scales: int = len(scale_factors)

avg_allocs_sweep: dict[int, pd.Series] = {}

robust_allocs_sweep: dict[int, pd.Series] = {}

for k in scale_factors:

# Scale attribution alpha by k (in log-space: add log(k))

mu_alpha_k = base_mu_alpha_attr + np.log(k)

model_k = build_response_model(

mu_alpha=mu_alpha_k,

sigma_alpha=model_configs["attribution"]["sigma_alpha"],

mu_lam=model_configs["attribution"]["mu_lam"],

sigma_lam=model_configs["attribution"]["sigma_lam"],

coords=coords,

n_dates=n_dates,

n_ch=n_ch,

)

with model_k:

idata_k = pm.sample_prior_predictive(samples=500, random_seed=seed)

idata_k.add_groups(posterior=idata_k.prior)

# Attribution-optimal allocation at this scale

wrapper_k = CustomModelWrapper(

base_model=model_k, idata=idata_k, channels=channels,

)

opt_k = BudgetOptimizer(model=wrapper_k, num_periods=n_future)

alloc_k, _ = opt_k.allocate_budget(

total_budget=TOTAL_BUDGET, budget_bounds=bounds,

)

if hasattr(alloc_k, "to_series"):

alloc_k = alloc_k.to_series()

elif not isinstance(alloc_k, pd.Series):

alloc_k = pd.Series(np.array(alloc_k).flatten(), index=channels)

# Merge at this scale: regression + experiment (fixed) + attribution_k

merged_k = BuildMergedModel(

models=[wrappers["regression"], wrappers["experiment"], wrapper_k],

prefixes=["regression", "experiment", "attribution"],

merge_on="channel_data",

)

merged_k.num_periods = n_future

merged_k.channel_columns = channels

# --- Averaged-model optimisation at this scale ---

with merged_k.model:

pm.Deterministic("averaged_total_contribution", (

merged_k.model["regression_total_contribution"]

+ merged_k.model["experiment_total_contribution"]

+ merged_k.model["attribution_total_contribution"]

) / 3)

avg_opt_k = BudgetOptimizer(

model=merged_k, num_periods=n_future,

response_variable="averaged_total_contribution",

)

alloc_avg_k, _ = avg_opt_k.allocate_budget(

total_budget=TOTAL_BUDGET, budget_bounds=bounds,

)

if hasattr(alloc_avg_k, "to_series"):

alloc_avg_k = alloc_avg_k.to_series()

elif not isinstance(alloc_avg_k, pd.Series):

alloc_avg_k = pd.Series(np.array(alloc_avg_k).flatten(), index=channels)

avg_allocs_sweep[k] = alloc_avg_k

# --- Minimax regret optimisation at this scale ---

# v_star for the scaled attribution model

attr_eval_dist = opt_k.extract_response_distribution("total_contribution")

attr_eval_fn = pytensor_function([opt_k._budgets_flat], pt.mean(attr_eval_dist))

v_star_attr_k = float(attr_eval_fn(alloc_k.values))

v_stars_sweep = {}

for sweep_name in ["regression", "experiment"]:

v_stars_sweep[sweep_name] = float(eval_fns[sweep_name](optimal_allocations[sweep_name].values))

with merged_k.model:

regret_vector_k = pt.stack([

1.0 - merged_k.model["regression_total_contribution"] / v_stars_sweep["regression"],

1.0 - merged_k.model["experiment_total_contribution"] / v_stars_sweep["experiment"],

1.0 - merged_k.model["attribution_total_contribution"] / v_star_attr_k,

])

pm.Deterministic("regret_vector", regret_vector_k)

def minimax_regret_utility(samples, budgets):

mean_regrets = pt.mean(samples, axis=0)

return -pt.max(mean_regrets)

rob_opt_k = BudgetOptimizer(

model=merged_k, num_periods=n_future,

response_variable="regret_vector",

utility_function=minimax_regret_utility,

)

alloc_rob_k, _ = rob_opt_k.allocate_budget(

total_budget=TOTAL_BUDGET, budget_bounds=bounds,

)

if hasattr(alloc_rob_k, "to_series"):

alloc_rob_k = alloc_rob_k.to_series()

elif not isinstance(alloc_rob_k, pd.Series):

alloc_rob_k = pd.Series(np.array(alloc_rob_k).flatten(), index=channels)

robust_allocs_sweep[k] = alloc_rob_k

# print(f"k={k:2d} | Avg: {alloc_avg_k.values.round(1)} | Robust: {alloc_rob_k.values.round(1)}")

fig, ax = plt.subplots(figsize=(8, 5))

for ch_idx, ch in enumerate(channels):

vals = [avg_allocs_sweep[k][ch]/TOTAL_BUDGET for k in scale_factors]

ax.plot(

scale_factors, vals,

marker="o", label=ch.capitalize(), color=f"C{ch_idx}", linewidth=2,

)

ax.set(

title="Averaged Model: Allocation Drifts With Attribution Scale",

xlabel="Attribution scale multiplier (k×)",

ylabel=f"Budget share (total = {TOTAL_BUDGET:.0f})",

)

ax.legend(fontsize=8)

ax.grid(True, alpha=0.3)

plt.show()

The result is damning. As one model’s scale increases from 1× to 10×, the averaged-model allocation pivots steadily toward that model’s preferred channels — the remaining views get progressively drowned out. This isn’t specific to attribution; any model whose average response grows will hijack the consensus. The “consensus” isn’t a consensus; it’s a hostage negotiation where the biggest number always wins.

The practical lesson

If your measurement systems operate at different scales — and they almost certainly do — averaging their outputs gives disproportionate influence to the system with the largest numbers. This is not a theoretical concern. Platform attribution routinely reports 5–15× more “conversions” than incrementality tests because it counts every touchpoint, not just the causal ones. Any aggregation method that doesn’t account for this will systematically over-invest in whatever the attribution dashboard recommends.

The evidence is clear. Averaging doesn’t just lack a meaningful interpretation — it actively chases whatever system shouts the loudest numbers, producing allocations that swing wildly as measurement scale changes. We need a framework that acknowledges model disagreement without trying to combine model outputs into a single prediction.

This is the gap that decision theory fills. Instead of trying to synthesise one “true” model, we acknowledge model uncertainty and choose the action that performs best given that uncertainty. We don’t combine the models — we combine their implications for decisions.

The Solution: Minimax Regret

Let’s formalise our situation. We have:

- A set of possible actions a \in \mathcal{A} (budget allocations across channels)

- A set of possible states of the world m \in \mathcal{M} (which model is correct)

- A payoff function V(a, m) that gives the expected response when action a is taken and model m is the true one

For each model m, there exists an optimal action a_m^* = \arg\max_a V(a, m) — the allocation we’d choose if we knew model m was correct.

The normalised regret of choosing action a when model m is true is the fraction of optimal value we leave on the table:

R(a, m) = 1 - \frac{V(a, m)}{V(a_m^*, m)}

Normalised regret lives in [0, 1]. Zero means we chose perfectly for that model. A value of 0.15 means we captured only 85% of what was achievable. Crucially, normalised regret is scale-invariant: if model m’s response is multiplied by any constant k, both numerator and denominator of the ratio V/V^* scale identically, leaving R unchanged. This property is essential when our models operate at different magnitudes — and it’s exactly why the right panel of the sensitivity plot held steady.

The minimax regret strategy chooses the action that minimizes the worst-case regret across all possible models:

a^{MR} = \arg\min_{a \in \mathcal{A}} \max_{m \in \mathcal{M}} R(a, m)

In words: find the allocation such that no matter which model turns out to be correct, our regret is as small as possible.

Why minimax regret?

This criterion has several compelling properties for our marketing setting:

No model weighting required. Unlike Bayesian Model Averaging, we don’t need to assign probabilities to each model being “correct.” We simply protect against the worst case.

Handles incommensurable models. We never combine the models’ parameters — we only evaluate each model’s response to the same allocation. The normalised regret is always computed within a single model’s framework, and because it measures the fraction of optimal value lost, it is invariant to the absolute scale of each model’s response.

Robust to model error. The resulting allocation hedges against all models, ensuring we never make a catastrophically bad decision under any of them.

Established theory. Minimax regret was formalised by Leonard Savage (1951) and connects directly to Distributionally Robust Optimisation (DRO) in modern operations research and to robust portfolio allocation in finance.

Portfolio analogy

Think of minimax regret as the decision-theory equivalent of portfolio diversification. Just as a diversified portfolio protects against uncertainty in individual stock returns, a minimax-regret allocation protects against uncertainty in which model is correct.

The Robust Allocation in Practice

For each model, the optimal response V^*(m) is the maximum achievable contribution — what we’d get if we knew that model was correct and optimised perfectly for it.

Code

v_stars = {}

for name in model_configs:

v_star = float(eval_fns[name](optimal_allocations[name].values))

v_stars[name] = v_star

# print(f"V* ({name}): {v_star:.4f}")These are the best possible outcomes under each model. Any other allocation will achieve less under that model, resulting in positive regret. Let’s evaluate every candidate allocation under every model to construct the regret matrix.

Code

# Gather all candidate allocations

candidate_allocations = {

"Regression\nOptimal": optimal_allocations["regression"],

"Experiment\nOptimal": optimal_allocations["experiment"],

"Attribution\nOptimal": optimal_allocations["attribution"],

"Averaged\nModel": naive_avg,

}

# Build the response and regret matrices

response_matrix = pd.DataFrame(

index=candidate_allocations.keys(),

columns=[n.capitalize() for n in model_configs.keys()],

dtype=float,

)

regret_matrix = response_matrix.copy()

for alloc_name, alloc in candidate_allocations.items():

alloc_vals = np.array(alloc).flatten()

for model_name in model_configs:

v = float(eval_fns[model_name](alloc_vals))

response_matrix.loc[alloc_name, model_name.capitalize()] = v

regret_matrix.loc[alloc_name, model_name.capitalize()] = 1.0 - v / v_stars[model_name]

# print("=== Response Matrix (expected contribution) ===")

# print(response_matrix.round(2).to_string())

# print()

# print("=== Normalised Regret Matrix (fraction of optimal lost) ===")

# print(regret_matrix.round(4).to_string())

# Add max regret column

regret_display = regret_matrix.copy()

regret_display["Max Regret"] = regret_display.max(axis=1)

fig, ax = plt.subplots(figsize=(10, 5))

sns.heatmap(

regret_display.astype(float),

annot=True,

fmt=".1%",

cmap="YlOrRd",

linewidths=0.5,

ax=ax,

vmin=0.0,

vmax=regret_display.values.max() * 1.2,

)

ax.set(

title="Normalised Regret: Fraction of Optimal Value Lost Under Each Scenario",

xlabel="If this model is correct...",

ylabel="If we choose this allocation...",

)

plt.show()

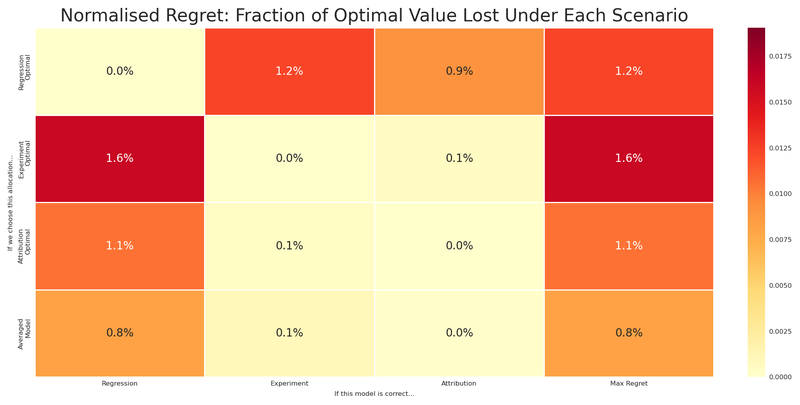

Read this matrix carefully:

- Each row is a candidate allocation (what we might choose).

- Each column is a scenario (which model turns out to be correct).

- Each cell is the normalised regret — the fraction of optimal value lost. A value of 0.15 means we capture only 85% of what was achievable under that model.

- The rightmost column is the maximum normalised regret: the worst-case scenario for each allocation.

Notice that each model’s optimal allocation has zero regret under its own model (by definition), but potentially large regret under the other models. The regression-optimal allocation gets hammered if the experiment model is correct. The experiment-optimal allocation suffers if regression or attribution is right.

The averaged model? Pulled toward attribution’s inflated scale, it mimics the attribution-optimal allocation — good when attribution is right, but exposed when it isn’t. It doesn’t hedge; it follows the loudest signal. And as we showed, the number it optimised has no coherent physical interpretation.

Can we do better?

We can solve the minimax regret problem directly: find the allocation that minimizes the maximum regret across all three models.

a^{MR} = \arg\min_{a} \max_{m \in \{\text{reg}, \text{exp}, \text{attr}\}} \left[ 1 - \frac{V(a, m)}{V^*(m)} \right]

subject to:

\sum_{c} a_c = B, \quad a_c \geq 0 \quad \forall c

Let’s verify by evaluating the robust allocation’s regret under each model.

Code

with merged.model:

regret_vector = pt.stack([

1.0 - merged.model[f"{name}_total_contribution"] / v_stars[name]

for name in model_configs

])

pm.Deterministic("regret_vector", regret_vector)

def minimax_regret_utility(samples, budgets):

mean_regrets = pt.mean(samples, axis=0)

return -pt.max(mean_regrets)

robust_optimizer = BudgetOptimizer(

model=merged,

num_periods=n_future,

response_variable="regret_vector",

utility_function=minimax_regret_utility,

)

robust_allocation, result_robust = robust_optimizer.allocate_budget(

total_budget=TOTAL_BUDGET,

budget_bounds=bounds,

)

if hasattr(robust_allocation, "to_series"):

robust_allocation = robust_allocation.to_series()

elif not isinstance(robust_allocation, pd.Series):

robust_allocation = pd.Series(np.array(robust_allocation).flatten(), index=channels)

# print(f"Optimisation success: {result_robust.success}")

# print(f"Maximum normalised regret (minimax): {result_robust.fun:.4f}")

# print(f"\nRobust allocation:")

# for ch in channels:

# # print(f" {ch}: {robust_allocation[ch]:.2f}")

# print(f" Total: {robust_allocation.sum():.2f}")

robust_vals = robust_allocation.values

naive_vals = naive_avg.values

# print("Robust allocation normalised regret under each model:")

robust_regrets = []

naive_regrets = []

for name in model_configs:

v = float(eval_fns[name](robust_vals))

regret = 1.0 - v / v_stars[name]

robust_regrets.append(regret)

naive_regrets.append(1.0 - float(eval_fns[name](naive_vals)) / v_stars[name])

# print(f" {name}: V={v:.4f}, Normalised regret={regret:.4f}")

robust_max_regret = max(robust_regrets)

naive_max_regret = max(naive_regrets)

# print(f"\nMax normalised regret — Robust: {robust_max_regret:.4f} | Averaged model: {naive_max_regret:.4f}")

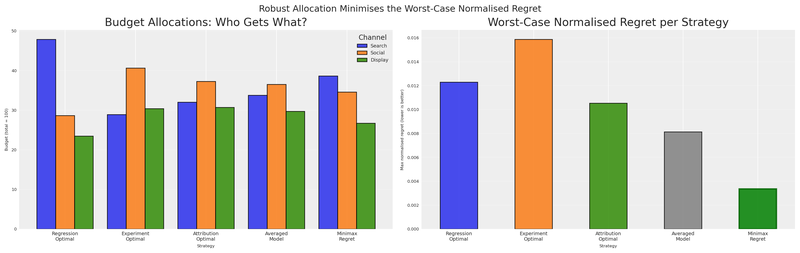

# print(f"Improvement: {((naive_max_regret - robust_max_regret) / naive_max_regret * 100):.1f}% reduction in worst-case regret")The robust allocation achieves a lower maximum normalised regret than the averaged model — and dramatically lower than any single model’s optimal. It hedges across models, never betting everything on one view being correct.

Let’s put everything together and compare all five allocations: the three model-specific optima, the averaged-model optimum, and the minimax-regret robust allocation.

Code

# Add robust allocation to candidates

all_allocations = {

"Regression\nOptimal": optimal_allocations["regression"],

"Experiment\nOptimal": optimal_allocations["experiment"],

"Attribution\nOptimal": optimal_allocations["attribution"],

"Averaged\nModel": naive_avg,

"Minimax\nRegret": robust_allocation,

}

# Full regret matrix

full_regret = pd.DataFrame(

index=all_allocations.keys(),

columns=[n.capitalize() for n in model_configs.keys()],

dtype=float,

)

for alloc_name, alloc in all_allocations.items():

alloc_vals = np.array(alloc).flatten()

for model_name in model_configs:

v = float(eval_fns[model_name](alloc_vals))

full_regret.loc[alloc_name, model_name.capitalize()] = 1.0 - v / v_stars[model_name]

full_regret["Max Regret"] = full_regret[[c.capitalize() for c in model_configs]].max(axis=1)

# print("=== Full Normalised Regret Matrix ===")

# print(full_regret.round(4).to_string())

fig, axes = plt.subplots(nrows=1, ncols=2, figsize=(16, 5))

# Panel 1: Allocations

alloc_compare = pd.DataFrame(

{name: alloc for name, alloc in all_allocations.items()}

).T

alloc_compare.columns = [ch.capitalize() for ch in channels]

alloc_compare.plot(kind="bar", ax=axes[0], edgecolor="black", alpha=0.85, width=0.8)

axes[0].set(

title="Budget Allocations: Who Gets What?",

xlabel="Strategy",

ylabel=f"Budget (total = {TOTAL_BUDGET:.0f})",

)

axes[0].legend(title="Channel", fontsize=7, loc="upper right")

axes[0].set_xticklabels(axes[0].get_xticklabels(), rotation=0, fontsize=7)

axes[0].grid(True, axis="y", alpha=0.3)

# Panel 2: Max regret

max_regrets = full_regret["Max Regret"].astype(float)

colors = ["C0", "C1", "C2", "grey", "green"]

max_regrets.plot(kind="bar", ax=axes[1], color=colors, edgecolor="black", alpha=0.85)

axes[1].set(

title="Worst-Case Normalised Regret per Strategy",

xlabel="Strategy",

ylabel="Max normalised regret (lower is better)",

)

axes[1].set_xticklabels(axes[1].get_xticklabels(), rotation=0, fontsize=7)

axes[1].grid(True, axis="y", alpha=0.3)

# Highlight the minimax regret bar

axes[1].patches[-1].set_edgecolor("darkgreen")

axes[1].patches[-1].set_linewidth(2)

fig.suptitle("Robust Allocation Minimises the Worst-Case Normalised Regret", fontsize=13)

plt.show()

The right panel tells the whole story. Every model-specific allocation has a tall bar — large worst-case normalised regret if it turns out to be wrong. The averaged model, pulled toward attribution’s preferred channels, carries worst-case exposure that a proper hedge can avoid. The minimax regret allocation (green) has the smallest worst-case normalised regret.

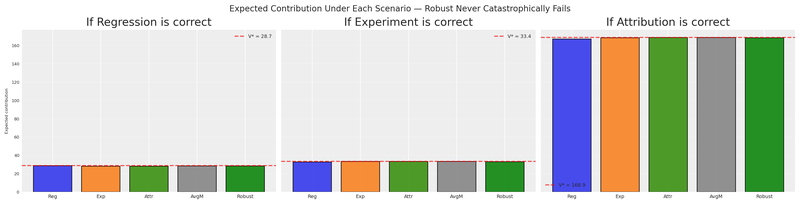

Let’s also visualise how each strategy performs under each model, looking not just at the regret but at the actual expected contribution.

Code

full_response = pd.DataFrame(

index=all_allocations.keys(),

columns=[n.capitalize() for n in model_configs.keys()],

dtype=float,

)

for alloc_name, alloc in all_allocations.items():

alloc_vals = np.array(alloc).flatten()

for model_name in model_configs:

v = float(eval_fns[model_name](alloc_vals))

full_response.loc[alloc_name, model_name.capitalize()] = v

fig, axes = plt.subplots(nrows=1, ncols=3, figsize=(16, 4), sharey=True)

colors_alloc = ["C0", "C1", "C2", "grey", "green"]

for idx, model_name in enumerate(model_configs):

ax = axes[idx]

model_label = model_name.capitalize()

values = full_response[model_label].astype(float)

bars = ax.bar(

range(len(values)),

values.values,

color=colors_alloc,

edgecolor="black",

alpha=0.85,

)

ax.axhline(

v_stars[model_name],

color="red",

linestyle="--",

alpha=0.7,

label=f"V* = {v_stars[model_name]:.1f}",

)

ax.set(

title=f"If {model_label} is correct",

xlabel="",

ylabel="Expected contribution" if idx == 0 else "",

)

ax.set_xticks(range(len(values)))

ax.set_xticklabels(

["Reg", "Exp", "Attr", "AvgM", "Robust"],

fontsize=7,

)

ax.legend(fontsize=7)

ax.grid(True, axis="y", alpha=0.3)

fig.suptitle(

"Expected Contribution Under Each Scenario — Robust Never Catastrophically Fails",

fontsize=12,

)

plt.show()

The robust allocation (green bar) is never the worst under any model. It may not be the best in any single scenario, but it’s consistently competitive. That’s the power of minimax regret — it sacrifices the possibility of being perfect in exchange for the guarantee of never being terrible.

Scale invariance: the final proof

Earlier we saw that averaging collapses when one model’s scale changes. Does minimax regret survive the same test? We already computed the robust allocations at every scale factor during the sensitivity sweep. Let’s put both strategies side by side.

Code

fig, axes = plt.subplots(nrows=1, ncols=2, figsize=(14, 5), sharey=True)

# Panel 1: Averaged model

ax = axes[0]

for ch_idx, ch in enumerate(channels):

vals = [avg_allocs_sweep[k][ch]/TOTAL_BUDGET for k in scale_factors]

ax.plot(

scale_factors, vals,

marker="o", label=ch.capitalize(), color=f"C{ch_idx}", linewidth=2,

)

ax.set(

title="Averaged Model: Allocation Drifts With Scale",

xlabel="Attribution scale multiplier (k×)",

ylabel=f"Budget share (total = {TOTAL_BUDGET:.0f})",

)

ax.legend(fontsize=8)

ax.grid(True, alpha=0.3)

# Panel 2: Minimax regret

ax = axes[1]

for ch_idx, ch in enumerate(channels):

vals = [robust_allocs_sweep[k][ch]/TOTAL_BUDGET for k in scale_factors]

ax.plot(

scale_factors, vals,

marker="s", label=ch.capitalize(), color=f"C{ch_idx}", linewidth=2,

)

ax.set(

title="Minimax Regret: Allocation Remains Stable",

xlabel="Attribution scale multiplier (k×)",

ylabel="",

)

ax.legend(fontsize=8)

ax.grid(True, alpha=0.3)

fig.suptitle(

"Sensitivity to Attribution Scale: Averaging Chases Volume, Regret Holds Steady",

fontsize=12,

)

plt.show()

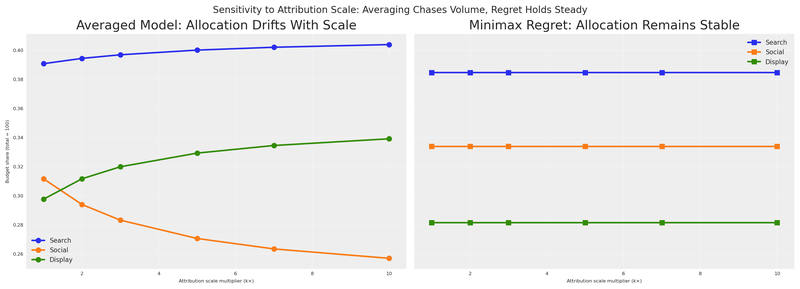

The contrast is stark. The left panel — the same averaging drift we saw before — shows allocations that are hostage to whichever model reports the largest numbers. The right panel barely moves. Normalised regret 1 - V/V^* is a ratio: if attribution’s entire response surface is multiplied by k, both V(a, m) and V^*(m) scale identically, and the ratio cancels. Scale invariance is not a coincidence of this particular example; it is a structural guarantee of the normalised formulation.

Scale-invariance guarantee

Because normalised regret is a ratio, multiplying any model’s entire response surface by a constant leaves the regret unchanged. In plain language: all measurement systems are treated on equal footing, none of them is prefer over the other, they have the same weight.

Considerations

Let’s crystallise this into a repeatable process and discuss when — and when not — to reach for this tool. Any marketing analytics team can follow this process:

- Gather your views. Collect the parameter estimates (or full posteriors) from each measurement system. Any view of reality — attribution dashboards, experimental lift estimates, regression coefficients — can become a PyMC model.

- Optimise individually using the

BudgetOptimizerto find the optimal allocation under each view. This gives you the candidate allocations and the V^*(m) benchmarks. - Merge the models with

BuildMergedModelso all views share a singlechannel_datainput — one computational graph, every response surface accessible. - Compute the normalised regret matrix by cross-evaluating every allocation under every model.

- Solve for the robust allocation by minimising the worst-case regret entry with a custom utility function in the

BudgetOptimizer. - Present to stakeholders. Show the regret matrix and the comparison plot. The pitch: “This allocation leaves the least value on the table no matter which model turns out to be correct.”

Code

# Summary table for the presentation

summary = pd.DataFrame(

{name: alloc for name, alloc in all_allocations.items()}

).T

summary.columns = [ch.capitalize() for ch in channels]

summary["Max Norm. Regret"] = full_regret["Max Regret"].values

summary.index = ["Regression", "Experiment", "Attribution", "Averaged Model", "Minimax Regret"]

summary = summary.round(4)

# print("=== Executive Summary: Budget Allocation Strategies ===")

# print(summary.to_string())When to use minimax regret

Minimax regret is most valuable when:

- You have multiple measurement systems that produce contradictory results.

- You cannot assign reliable probabilities to which model is correct.

- The cost of being wrong is asymmetric or severe — you’d rather avoid catastrophic failure than chase the best possible outcome.

- Stakeholders need a single, defensible recommendation from a diverse set of inputs.

Broader mathematical context

Minimax regret is not an isolated trick; it connects deeply to broader frameworks in operations research and finance.

The minimax regret formulation we’ve used is a special case of Distributionally Robust Optimisation (DRO), a framework widely used in finance and operations research. In DRO, the decision-maker optimises against the worst-case distribution within an ambiguity set — a collection of plausible probability models. Our three models form a discrete ambiguity set:

\mathcal{P} = \{P_{\text{reg}}, P_{\text{exp}}, P_{\text{attr}}\}

The DRO problem is:

\max_{a} \min_{P \in \mathcal{P}} \mathbb{E}_P[V(a)]

This is the maximin (maximize the minimum expected value) variant. Our minimax regret formulation is closely related but focuses on regret rather than absolute performance — a subtle but important distinction when models produce different scales of response.

If you work in finance, the parallel to portfolio theory is exact:

| Marketing | Finance |

|---|---|

| Budget allocation across channels | Portfolio allocation across assets |

| Each model’s belief about channel returns | Each analyst’s belief about asset returns |

| Minimax regret allocation | Robust portfolio that hedges model risk |

| Model uncertainty | Parameter uncertainty / estimation risk |

In the Black-Litterman model, multiple “views” about asset returns are combined with market equilibrium. Our approach is similar in spirit but does not require assigning confidence weights to each view — the minimax regret criterion handles the combination implicitly.

Limitations

- Minimax regret is conservative by design. It optimises for the worst case, which means it may sacrifice upside when one model is clearly superior.

- With many models, the worst case can dominate and produce overly diversified allocations. In practice, limit your model set to 3–5 genuinely distinct views.

- The approach treats all models as equally plausible. If you have strong reasons to trust one model over others, weighted regret or Bayesian model averaging may be more appropriate.

Extensions

- Weighted minimax regret: Assign confidence weights w_m to each model and minimize \max_m w_m \cdot R(a, m). This bridges the gap between pure minimax and Bayesian model averaging.

- Risk-averse evaluation: Instead of using the posterior mean for V(a, m), use a lower quantile (e.g., 5th percentile) for an even more conservative allocation.

- Time-varying views: If model reliability changes over time (e.g., the experiment was recent but the MMM covers years), incorporate temporal weighting.

- Bayesian Model Selection: Use marginal likelihoods to assign model probabilities, then combine with minimax for a hybrid approach.

Conclusions

Different measurement systems answer different questions. A regression-based MMM, a controlled experiment, and an attribution model each capture a different facet of marketing effectiveness. Their disagreement is not a bug — it’s a feature of measuring a complex system from multiple angles.

You cannot average apples, oranges, and bananas. Averaging model outputs across different measurement systems is a dimensional error. Even when it produces a distribution, no draw from that distribution corresponds to any real-world outcome. The “consensus model” is a Frankenstein with no coherent interpretation.

Scale asymmetry breaks naive aggregation. When measurement systems operate at different scales — as they invariably do in practice — averaging lets the loudest system dominate. The sensitivity analysis confirms that averaged-model allocations shift dramatically as one model’s scale changes by an order of magnitude, while minimax-regret allocations remain stable.

Decision theory fills the gap. When models disagree and you can’t combine their estimates, you can still combine their implications for decisions. Minimax regret finds the allocation that minimizes the worst-case normalised opportunity cost across all models — the fraction of optimal value left on the table.

The robust allocation hedges against model error. By optimising for the worst case, minimax regret produces allocations that are competitive under every model — never perfect, but never catastrophic. This is the portfolio diversification principle applied to model uncertainty.

The workflow is practical and presentable. Optimise under each model, compute the regret matrix, solve for the minimax allocation, and present the comparison. Stakeholders can see exactly how each strategy performs under each scenario — no black boxes.

Decisions are hard even with a single number. With multiple contradictory numbers, they seem impossible. But with the right framework — treating models as views and allocations as actions — we can navigate the contradiction and find strategies that are robust to our uncertainty about which view is correct.

The models don’t need to agree. We just need a decision theory that doesn’t require them to.

Recommended readings:

- Minimax Regret — Wikipedia

- Distributionally Robust Optimization — Rahimian & Mehrotra (2019)

- Black-Litterman Model — Wikipedia

- PyMC-Marketing documentation

- Savage, L.J. (1951). The Theory of Statistical Decision

Version information

Code

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc_marketing,pytensorLast updated: Tue Jul 14 2026

Python implementation: CPython

Python version : 3.11.8

IPython version : 8.30.0

pymc_marketing: 0.17.1

pytensor : 2.37.0

pytensor : 2.37.0

pymc : 5.27.1

numpy : 2.1.3

seaborn : 0.13.2

arviz : 0.21.0

preliz : 0.20.0

pandas : 2.2.3

matplotlib : 3.10.1

pymc_marketing: 0.17.1

Watermark: 2.5.0